Bank Interest

Muslim Knowledge Guide Al-Azhar: Bank Interest, Riba Fatwa and Islamic Finance Debate

Articles • yusuf908 posted the article • 0 comments • 119 views • 2026-05-23 02:38

Reposted from the web

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

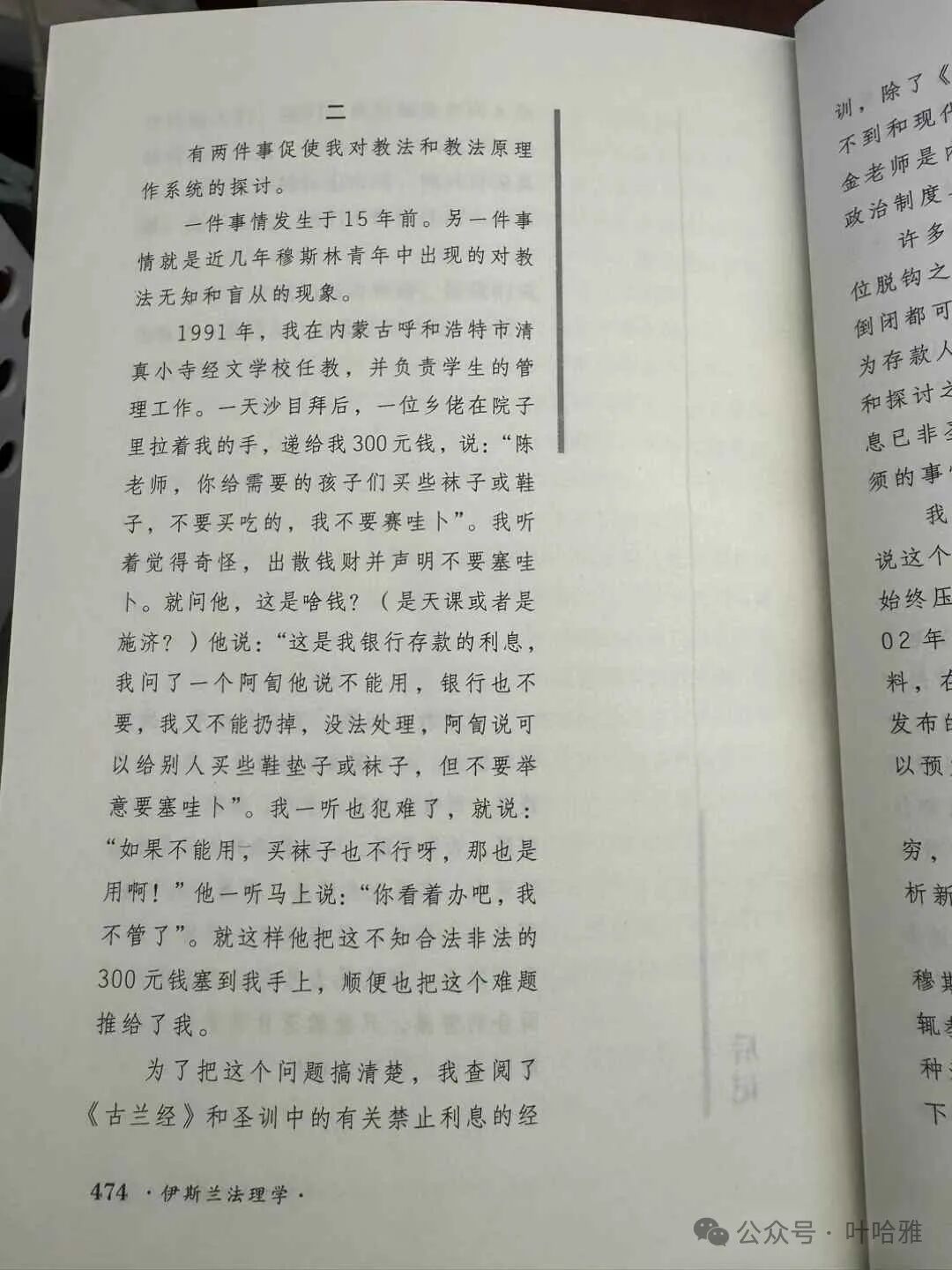

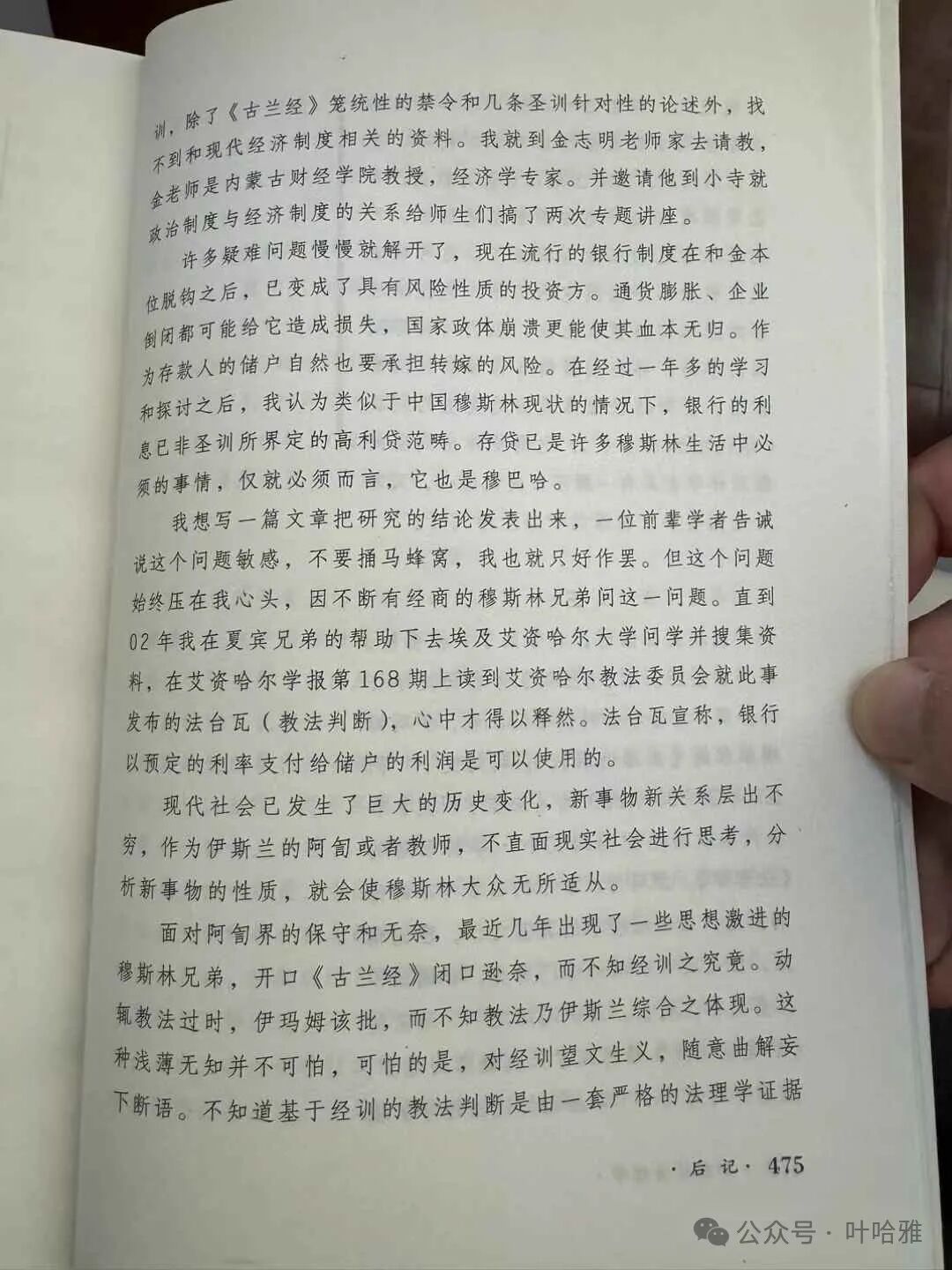

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.

This set profit rate can go up or down over time. For example, an investment project might start with a 4% return, grow to over 15%, and then recently drop back to near 10%.

The people who set these rates and manage their changes must follow government rules. Setting a fixed number in advance—especially in these times when honesty is rare—benefits both the investors and the bank.

Investors benefit from stable profit rates, which helps them plan their lives. Bank managers benefit from performance incentives, which push them to work harder to maximize profits and keep the bank profitable even after paying the investors their set returns. What if the bank loses money during that time? How can it set a profit rate in advance? The answer is that a bank might lose money on one investment but make a profit on many others, which covers the loss.

In short: it is allowed for someone to invest money through an institution into a bank or other financial firm with a pre-set profit. There is nothing suspicious about it. This type of transaction is judged by its benefits and is not considered associating partners with Allah (shirk). Therefore, investing money in a bank with a pre-agreed profit or return is allowed and causes no harm. Allah knows best.

What does this religious ruling (fatwa) not say?

Please note that this fatwa does not explicitly state that all bank interest is halal.

Dr. Tantawi has clearly stated elsewhere that interest on bank deposits is riba, and interest on bank loans is also riba. (See Mucamalat al-Bunuk..., 2001, pp. 139-142)

There are three points of contention here.

First, are funds held for business operations considered deposits?

Second, are funds borrowed for business operations considered loans?

Third, is it forbidden to pre-determine the profit for one party in an investment activity?

There is little disagreement regarding deposits.

There is substantial disagreement regarding loans:

Abdullah Al-Najjar explains Dr. Tantawi's position as follows:

Funds given to a bank cannot be seen as a form of loan because the bank has no need, and only those in need apply for loans. Anas ibn Malik reported that the Prophet said: 'On the night of the Ascension, I saw written on the gate of Paradise: Charity is rewarded tenfold, and a loan is rewarded eighteenfold.' I said: 'O Jibril!' Why is borrowing more expensive than giving charity? The angel Jibril said: 'Because a beggar asks when they still have something, but a borrower only asks when they are in urgent need.' — Sunan Ibn Majah

Therefore, if a transaction is not a loan, bank customers must be seen as investors who intend to seek profit from the bank (the bank announces the return rate they pay, and customers choose the bank they prefer).

Jurists believe that once deposit funds are used, they are promised, and because holding a guarantee (like a loan) is more reliable than holding a trust (like a deposit), the deposit contract becomes a loan, and any increase is forbidden interest (riba).

the 'preset profit' in profit-sharing (mudaraba) is the core of what this Islamic law forbids.

Al-Qaradawi and many others believe that the hadith regarding sharecropping (muzara'ah) provides the basis for the prohibition. The Sharia committee mentioned the claim of 'consensus' put forward by Ibn Qudamah in Al-Mughni and confirmed that this 'consensus' is as binding as the classical texts.

The 14th session of the Fiqh Academy, January 2003, Decision #133 (7/14), pages 20-24.

Religious law and secular law describe the relationship between a depositor and a bank as a loan relationship, not an agency relationship. In contrast, an investment agency is where an agent invests funds on behalf of a principal in exchange for a fixed wage or a share of the profits. In this regard, religious scholars have a consensus that the principal owns the investment funds and therefore has the right to receive investment gains and is responsible for losses, while the agent has the right to receive a fixed wage under the conditions set by the agency. Therefore, a traditional bank is not an investment agent for the depositor. The bank receives funds from the depositor and uses them, thereby guaranteeing said funds and making them a loan. In this regard, the loan must be repaid at face value without any increase.

For centuries, jurists from all schools have agreed that you cannot pre-set investment profits in any partnership, whether as a fixed amount or a percentage of the capital. This ruling is based on the idea that pre-setting profits guarantees the principal, which goes against the nature of a partnership where you must share both profits and losses. This consensus is well-established and has no reported disagreements. In this regard, Ibn Qudamah wrote in Al-Mughni (Volume 3, page 34): All scholars agree that if one or both parties set a known amount of profit, the partnership (qirad or mudaraba) becomes invalid. The consensus of religious scholars is itself a legal proof.

Pre-specifying profits

Dr. Tantawi and his supporters rejected the loan issue and held a long discussion on the problem of pre-set profits. Dr. Tantawi cited Abdul-Wahhab Khallaf and Dr. Ali Al-Khafif to support his view that it is inappropriate to limit investment institutions to traditional mudaraba, which has profit sharing but no specific profit amount.

The main argument for fixed profits

Tantawi (2001, page 131) quoted Khallaf (pages 94-104), Al-Khafif (pages 165-204), and others (pages 204-211) word for word, saying: In this era of corruption, dishonesty, and greed, not fixing profits as a percentage of capital would leave the principal at the mercy of the agents managing the investment funds, whether they are banks or other institutions.

Therefore, he and earlier scholars turned to the well-known issue of moral hazard, which is unrelated to profit distribution.

Second, once the loan or deposit argument is rejected, the remaining issue is how to handle the consensus theory in Al-Mughni and the hadith it is based on.

Is the claim of consensus accepted? Is it binding?

Does this decision have a basis in the Quran and Sunnah, or can it be overturned?

If a partnership is considered flawed because the profit margin is predetermined, does this make it forbidden interest (riba), or is it a permitted lease (ijara), such as whether a mutually agreed upon (though uncertain) wage payment is legal?

Hadith on tenant farming.

Hanzalah ibn Qays narrated: I asked Rafi ibn Khadij about renting land for gold and silver. Rafi replied: 'There is no harm in this. In the time of the Prophet, people rented land for the crops and straw that grew along the waterways. Sometimes there was a harvest, and sometimes there was none. People rented land this way, so the Prophet forbade it. As for rent that is fixed and guaranteed, there is no harm.'

— Sunan Ibn Majah

This hadith shows that it is forbidden to pre-arrange any geography, time, or quantity for land rented to tenant farmers. Jurists concluded that because of uncertainty, predetermined compensation for either party is not allowed. This ruling on tenant farming applies to other partnerships, including profit-sharing partnerships (mudaraba). Therefore, Ibn Qudamah believed that jurists reached a consensus that it is not allowed to pre-specify profits in a mudaraba.

Dr. Abdullah Al-Najjar wrote a detailed discussion on this hadith and the conclusions drawn from it. He argued that the prohibition does not stem from the condition of pre-specifying profit itself, but from the uncertainty (gharar) that could lead to disputes (citing the narrative and analysis in Al-Shawkani's Nayl Al-Awtar). On the other hand, he argued that this type of partnership is essentially an employment contract with an unknown reward, and is therefore full of uncertainty. However, a consensus ruling actually permits this contract (including profit sharing) despite the uncertainty (as Ibn Qudamah stated). Therefore, this type of partnership belongs to a category of contracts where uncertainty (including that caused by pre-specifying profit) is ignored, as long as it does not lead to legal disputes.

Dr. Al-Najjar presented many other arguments based on the analysis of Al-Shawkani and Ibn Qudamah. He said: This might be Rafi's own non-binding conclusion; it might be limited to specific types of tenant farming; Zayd ibn Thabit disagreed with this hadith, claiming it related to a specific incident where one person killed another (recorded by Abu Dawud); the hadith narrated by Ibn Umar suggests that renting land is permitted (recorded by Bukhari), which challenges the hadith; other companions of the Prophet, including Ibn Abbas and others, disagreed with Rafi's view. Ibn Qudamah said that some of Rafi's narrations differ from the consensus of the companions and must therefore be discarded.

At the Al-Azhar conference, Dr. Muhammad Rif'at Uthman presented a counter-argument. According to Al-Nawawi, the hadith does not forbid renting land for a fixed rent (which was the focus of previous arguments), but it does forbid pre-specifying profits.

Most jurists believe that a profit-sharing partnership (mudāraba) that is known to be flawed or invalid from the start is not allowed. Dr. Tantāwī focuses on the consensus view that when a mudāraba is considered flawed, such as when an investor's profit is specified in advance, the contract becomes an employment contract ('ijara). Under this, the entrepreneur or worker is entitled to a market wage, as noted by ibn al-Humām in Fath Al-Qadīr and Al-Shaficī in 'um. He summarizes this (2001, p. 133):

Therefore, we say that a bank investing for a pre-specified profit becomes an employee of the investor. The investor accepts the amount the bank gives them as their profit, and any excess profit, whatever it may be, is treated as the bank's wage. Thus, this type of transaction is free of interest (Ribā). In short, we cannot find any canonical text or convincing analogy that forbids specifying profit in advance as long as both parties agree.

Quotes from early jurists

Dr. Tantāwī (2001, p. 95) quotes Dr. Khallāf, who in turn quotes Muhammad Abduh's 1906 article in Manār (#9, p. 332): When a person gives their money to another for investment and receives a known profit, this does not constitute clearly forbidden Ribā, regardless of the pre-specified profit rate. This is because legal rules that disagree on forbidding pre-specified profit do not constitute the clear type of Ribā that ruins families. This type of transaction is beneficial to both the investor and the entrepreneur. In contrast, Ribā for the borrower is only due to need and is not their fault, while for the lender, Ribā leads to greed and a hardened heart. These two types of transactions cannot have the same legal status (hukm).

Dr. Khallāf, in Liwā' 'Islām (1951, #4 (11)), continues (quoted in the same, pp. 95-6): There is no evidence that profit cannot be specified in advance. Just as profit can be shared between two parties, the profit for one party can also be specified in advance. Such a condition might not align with the views of jurists, but it does not contradict any canonical text in the Quran or Sunnah.

Core argument

Dr. Khallaf summarizes the basis for the current Al-Azhar ruling as follows: The only objection to this type of transaction is the validity of mudāraba, which requires that profit must be set as a percentage share rather than a specific capital amount or percentage. My response to this objection is as follows: First, there is no evidence for this condition in the Quran or the Sunnah. We live in a very dishonest time now, and if we do not set a fixed profit for the investor, his partner will swallow up his wealth.

Second, if a mudāraba is considered flawed because it violates one of its conditions, the entrepreneur becomes an employee, and what he takes is considered a wage. There is no difference in calling it mudāraba or 'ijāra: it is a valid transaction that benefits the investor who cannot invest funds directly and benefits the entrepreneur who receives the funds. Therefore, this is a transaction that benefits both parties without harming either side or anyone else, and banning such a beneficial transaction will harm the Ummah.

Key points

Recent academic journals from Al-Azhar do allow certain types of bank interest to be used as investment profit.

This fatwa is at least a century old.

Most jurists oppose this fatwa.

A minority have questioned the authenticity, authority, and applicability of the hadith regarding sharecroppers.

A minority have questioned the logic of prohibiting the pre-specification of profit.

Can we still claim that a consensus exists?

If this issue is controversial, should we proceed with caution? Should we follow the view of the majority? view all

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.

This set profit rate can go up or down over time. For example, an investment project might start with a 4% return, grow to over 15%, and then recently drop back to near 10%.

The people who set these rates and manage their changes must follow government rules. Setting a fixed number in advance—especially in these times when honesty is rare—benefits both the investors and the bank.

Investors benefit from stable profit rates, which helps them plan their lives. Bank managers benefit from performance incentives, which push them to work harder to maximize profits and keep the bank profitable even after paying the investors their set returns. What if the bank loses money during that time? How can it set a profit rate in advance? The answer is that a bank might lose money on one investment but make a profit on many others, which covers the loss.

In short: it is allowed for someone to invest money through an institution into a bank or other financial firm with a pre-set profit. There is nothing suspicious about it. This type of transaction is judged by its benefits and is not considered associating partners with Allah (shirk). Therefore, investing money in a bank with a pre-agreed profit or return is allowed and causes no harm. Allah knows best.

What does this religious ruling (fatwa) not say?

Please note that this fatwa does not explicitly state that all bank interest is halal.

Dr. Tantawi has clearly stated elsewhere that interest on bank deposits is riba, and interest on bank loans is also riba. (See Mucamalat al-Bunuk..., 2001, pp. 139-142)

There are three points of contention here.

First, are funds held for business operations considered deposits?

Second, are funds borrowed for business operations considered loans?

Third, is it forbidden to pre-determine the profit for one party in an investment activity?

There is little disagreement regarding deposits.

There is substantial disagreement regarding loans:

Abdullah Al-Najjar explains Dr. Tantawi's position as follows:

Funds given to a bank cannot be seen as a form of loan because the bank has no need, and only those in need apply for loans. Anas ibn Malik reported that the Prophet said: 'On the night of the Ascension, I saw written on the gate of Paradise: Charity is rewarded tenfold, and a loan is rewarded eighteenfold.' I said: 'O Jibril!' Why is borrowing more expensive than giving charity? The angel Jibril said: 'Because a beggar asks when they still have something, but a borrower only asks when they are in urgent need.' — Sunan Ibn Majah

Therefore, if a transaction is not a loan, bank customers must be seen as investors who intend to seek profit from the bank (the bank announces the return rate they pay, and customers choose the bank they prefer).

Jurists believe that once deposit funds are used, they are promised, and because holding a guarantee (like a loan) is more reliable than holding a trust (like a deposit), the deposit contract becomes a loan, and any increase is forbidden interest (riba).

the 'preset profit' in profit-sharing (mudaraba) is the core of what this Islamic law forbids.

Al-Qaradawi and many others believe that the hadith regarding sharecropping (muzara'ah) provides the basis for the prohibition. The Sharia committee mentioned the claim of 'consensus' put forward by Ibn Qudamah in Al-Mughni and confirmed that this 'consensus' is as binding as the classical texts.

The 14th session of the Fiqh Academy, January 2003, Decision #133 (7/14), pages 20-24.

Religious law and secular law describe the relationship between a depositor and a bank as a loan relationship, not an agency relationship. In contrast, an investment agency is where an agent invests funds on behalf of a principal in exchange for a fixed wage or a share of the profits. In this regard, religious scholars have a consensus that the principal owns the investment funds and therefore has the right to receive investment gains and is responsible for losses, while the agent has the right to receive a fixed wage under the conditions set by the agency. Therefore, a traditional bank is not an investment agent for the depositor. The bank receives funds from the depositor and uses them, thereby guaranteeing said funds and making them a loan. In this regard, the loan must be repaid at face value without any increase.

For centuries, jurists from all schools have agreed that you cannot pre-set investment profits in any partnership, whether as a fixed amount or a percentage of the capital. This ruling is based on the idea that pre-setting profits guarantees the principal, which goes against the nature of a partnership where you must share both profits and losses. This consensus is well-established and has no reported disagreements. In this regard, Ibn Qudamah wrote in Al-Mughni (Volume 3, page 34): All scholars agree that if one or both parties set a known amount of profit, the partnership (qirad or mudaraba) becomes invalid. The consensus of religious scholars is itself a legal proof.

Pre-specifying profits

Dr. Tantawi and his supporters rejected the loan issue and held a long discussion on the problem of pre-set profits. Dr. Tantawi cited Abdul-Wahhab Khallaf and Dr. Ali Al-Khafif to support his view that it is inappropriate to limit investment institutions to traditional mudaraba, which has profit sharing but no specific profit amount.

The main argument for fixed profits

Tantawi (2001, page 131) quoted Khallaf (pages 94-104), Al-Khafif (pages 165-204), and others (pages 204-211) word for word, saying: In this era of corruption, dishonesty, and greed, not fixing profits as a percentage of capital would leave the principal at the mercy of the agents managing the investment funds, whether they are banks or other institutions.

Therefore, he and earlier scholars turned to the well-known issue of moral hazard, which is unrelated to profit distribution.

Second, once the loan or deposit argument is rejected, the remaining issue is how to handle the consensus theory in Al-Mughni and the hadith it is based on.

Is the claim of consensus accepted? Is it binding?

Does this decision have a basis in the Quran and Sunnah, or can it be overturned?

If a partnership is considered flawed because the profit margin is predetermined, does this make it forbidden interest (riba), or is it a permitted lease (ijara), such as whether a mutually agreed upon (though uncertain) wage payment is legal?

Hadith on tenant farming.

Hanzalah ibn Qays narrated: I asked Rafi ibn Khadij about renting land for gold and silver. Rafi replied: 'There is no harm in this. In the time of the Prophet, people rented land for the crops and straw that grew along the waterways. Sometimes there was a harvest, and sometimes there was none. People rented land this way, so the Prophet forbade it. As for rent that is fixed and guaranteed, there is no harm.'

— Sunan Ibn Majah

This hadith shows that it is forbidden to pre-arrange any geography, time, or quantity for land rented to tenant farmers. Jurists concluded that because of uncertainty, predetermined compensation for either party is not allowed. This ruling on tenant farming applies to other partnerships, including profit-sharing partnerships (mudaraba). Therefore, Ibn Qudamah believed that jurists reached a consensus that it is not allowed to pre-specify profits in a mudaraba.

Dr. Abdullah Al-Najjar wrote a detailed discussion on this hadith and the conclusions drawn from it. He argued that the prohibition does not stem from the condition of pre-specifying profit itself, but from the uncertainty (gharar) that could lead to disputes (citing the narrative and analysis in Al-Shawkani's Nayl Al-Awtar). On the other hand, he argued that this type of partnership is essentially an employment contract with an unknown reward, and is therefore full of uncertainty. However, a consensus ruling actually permits this contract (including profit sharing) despite the uncertainty (as Ibn Qudamah stated). Therefore, this type of partnership belongs to a category of contracts where uncertainty (including that caused by pre-specifying profit) is ignored, as long as it does not lead to legal disputes.

Dr. Al-Najjar presented many other arguments based on the analysis of Al-Shawkani and Ibn Qudamah. He said: This might be Rafi's own non-binding conclusion; it might be limited to specific types of tenant farming; Zayd ibn Thabit disagreed with this hadith, claiming it related to a specific incident where one person killed another (recorded by Abu Dawud); the hadith narrated by Ibn Umar suggests that renting land is permitted (recorded by Bukhari), which challenges the hadith; other companions of the Prophet, including Ibn Abbas and others, disagreed with Rafi's view. Ibn Qudamah said that some of Rafi's narrations differ from the consensus of the companions and must therefore be discarded.

At the Al-Azhar conference, Dr. Muhammad Rif'at Uthman presented a counter-argument. According to Al-Nawawi, the hadith does not forbid renting land for a fixed rent (which was the focus of previous arguments), but it does forbid pre-specifying profits.

Most jurists believe that a profit-sharing partnership (mudāraba) that is known to be flawed or invalid from the start is not allowed. Dr. Tantāwī focuses on the consensus view that when a mudāraba is considered flawed, such as when an investor's profit is specified in advance, the contract becomes an employment contract ('ijara). Under this, the entrepreneur or worker is entitled to a market wage, as noted by ibn al-Humām in Fath Al-Qadīr and Al-Shaficī in 'um. He summarizes this (2001, p. 133):

Therefore, we say that a bank investing for a pre-specified profit becomes an employee of the investor. The investor accepts the amount the bank gives them as their profit, and any excess profit, whatever it may be, is treated as the bank's wage. Thus, this type of transaction is free of interest (Ribā). In short, we cannot find any canonical text or convincing analogy that forbids specifying profit in advance as long as both parties agree.

Quotes from early jurists

Dr. Tantāwī (2001, p. 95) quotes Dr. Khallāf, who in turn quotes Muhammad Abduh's 1906 article in Manār (#9, p. 332): When a person gives their money to another for investment and receives a known profit, this does not constitute clearly forbidden Ribā, regardless of the pre-specified profit rate. This is because legal rules that disagree on forbidding pre-specified profit do not constitute the clear type of Ribā that ruins families. This type of transaction is beneficial to both the investor and the entrepreneur. In contrast, Ribā for the borrower is only due to need and is not their fault, while for the lender, Ribā leads to greed and a hardened heart. These two types of transactions cannot have the same legal status (hukm).

Dr. Khallāf, in Liwā' 'Islām (1951, #4 (11)), continues (quoted in the same, pp. 95-6): There is no evidence that profit cannot be specified in advance. Just as profit can be shared between two parties, the profit for one party can also be specified in advance. Such a condition might not align with the views of jurists, but it does not contradict any canonical text in the Quran or Sunnah.

Core argument

Dr. Khallaf summarizes the basis for the current Al-Azhar ruling as follows: The only objection to this type of transaction is the validity of mudāraba, which requires that profit must be set as a percentage share rather than a specific capital amount or percentage. My response to this objection is as follows: First, there is no evidence for this condition in the Quran or the Sunnah. We live in a very dishonest time now, and if we do not set a fixed profit for the investor, his partner will swallow up his wealth.

Second, if a mudāraba is considered flawed because it violates one of its conditions, the entrepreneur becomes an employee, and what he takes is considered a wage. There is no difference in calling it mudāraba or 'ijāra: it is a valid transaction that benefits the investor who cannot invest funds directly and benefits the entrepreneur who receives the funds. Therefore, this is a transaction that benefits both parties without harming either side or anyone else, and banning such a beneficial transaction will harm the Ummah.

Key points

Recent academic journals from Al-Azhar do allow certain types of bank interest to be used as investment profit.

This fatwa is at least a century old.

Most jurists oppose this fatwa.

A minority have questioned the authenticity, authority, and applicability of the hadith regarding sharecroppers.

A minority have questioned the logic of prohibiting the pre-specification of profit.

Can we still claim that a consensus exists?

If this issue is controversial, should we proceed with caution? Should we follow the view of the majority? view all

Reposted from the web

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.

This set profit rate can go up or down over time. For example, an investment project might start with a 4% return, grow to over 15%, and then recently drop back to near 10%.

The people who set these rates and manage their changes must follow government rules. Setting a fixed number in advance—especially in these times when honesty is rare—benefits both the investors and the bank.

Investors benefit from stable profit rates, which helps them plan their lives. Bank managers benefit from performance incentives, which push them to work harder to maximize profits and keep the bank profitable even after paying the investors their set returns. What if the bank loses money during that time? How can it set a profit rate in advance? The answer is that a bank might lose money on one investment but make a profit on many others, which covers the loss.

In short: it is allowed for someone to invest money through an institution into a bank or other financial firm with a pre-set profit. There is nothing suspicious about it. This type of transaction is judged by its benefits and is not considered associating partners with Allah (shirk). Therefore, investing money in a bank with a pre-agreed profit or return is allowed and causes no harm. Allah knows best.

What does this religious ruling (fatwa) not say?

Please note that this fatwa does not explicitly state that all bank interest is halal.

Dr. Tantawi has clearly stated elsewhere that interest on bank deposits is riba, and interest on bank loans is also riba. (See Mucamalat al-Bunuk..., 2001, pp. 139-142)

There are three points of contention here.

First, are funds held for business operations considered deposits?

Second, are funds borrowed for business operations considered loans?

Third, is it forbidden to pre-determine the profit for one party in an investment activity?

There is little disagreement regarding deposits.

There is substantial disagreement regarding loans:

Abdullah Al-Najjar explains Dr. Tantawi's position as follows:

Funds given to a bank cannot be seen as a form of loan because the bank has no need, and only those in need apply for loans. Anas ibn Malik reported that the Prophet said: 'On the night of the Ascension, I saw written on the gate of Paradise: Charity is rewarded tenfold, and a loan is rewarded eighteenfold.' I said: 'O Jibril!' Why is borrowing more expensive than giving charity? The angel Jibril said: 'Because a beggar asks when they still have something, but a borrower only asks when they are in urgent need.' — Sunan Ibn Majah

Therefore, if a transaction is not a loan, bank customers must be seen as investors who intend to seek profit from the bank (the bank announces the return rate they pay, and customers choose the bank they prefer).

Jurists believe that once deposit funds are used, they are promised, and because holding a guarantee (like a loan) is more reliable than holding a trust (like a deposit), the deposit contract becomes a loan, and any increase is forbidden interest (riba).

the 'preset profit' in profit-sharing (mudaraba) is the core of what this Islamic law forbids.

Al-Qaradawi and many others believe that the hadith regarding sharecropping (muzara'ah) provides the basis for the prohibition. The Sharia committee mentioned the claim of 'consensus' put forward by Ibn Qudamah in Al-Mughni and confirmed that this 'consensus' is as binding as the classical texts.

The 14th session of the Fiqh Academy, January 2003, Decision #133 (7/14), pages 20-24.

Religious law and secular law describe the relationship between a depositor and a bank as a loan relationship, not an agency relationship. In contrast, an investment agency is where an agent invests funds on behalf of a principal in exchange for a fixed wage or a share of the profits. In this regard, religious scholars have a consensus that the principal owns the investment funds and therefore has the right to receive investment gains and is responsible for losses, while the agent has the right to receive a fixed wage under the conditions set by the agency. Therefore, a traditional bank is not an investment agent for the depositor. The bank receives funds from the depositor and uses them, thereby guaranteeing said funds and making them a loan. In this regard, the loan must be repaid at face value without any increase.

For centuries, jurists from all schools have agreed that you cannot pre-set investment profits in any partnership, whether as a fixed amount or a percentage of the capital. This ruling is based on the idea that pre-setting profits guarantees the principal, which goes against the nature of a partnership where you must share both profits and losses. This consensus is well-established and has no reported disagreements. In this regard, Ibn Qudamah wrote in Al-Mughni (Volume 3, page 34): All scholars agree that if one or both parties set a known amount of profit, the partnership (qirad or mudaraba) becomes invalid. The consensus of religious scholars is itself a legal proof.

Pre-specifying profits

Dr. Tantawi and his supporters rejected the loan issue and held a long discussion on the problem of pre-set profits. Dr. Tantawi cited Abdul-Wahhab Khallaf and Dr. Ali Al-Khafif to support his view that it is inappropriate to limit investment institutions to traditional mudaraba, which has profit sharing but no specific profit amount.

The main argument for fixed profits

Tantawi (2001, page 131) quoted Khallaf (pages 94-104), Al-Khafif (pages 165-204), and others (pages 204-211) word for word, saying: In this era of corruption, dishonesty, and greed, not fixing profits as a percentage of capital would leave the principal at the mercy of the agents managing the investment funds, whether they are banks or other institutions.

Therefore, he and earlier scholars turned to the well-known issue of moral hazard, which is unrelated to profit distribution.

Second, once the loan or deposit argument is rejected, the remaining issue is how to handle the consensus theory in Al-Mughni and the hadith it is based on.

Is the claim of consensus accepted? Is it binding?

Does this decision have a basis in the Quran and Sunnah, or can it be overturned?

If a partnership is considered flawed because the profit margin is predetermined, does this make it forbidden interest (riba), or is it a permitted lease (ijara), such as whether a mutually agreed upon (though uncertain) wage payment is legal?

Hadith on tenant farming.

Hanzalah ibn Qays narrated: I asked Rafi ibn Khadij about renting land for gold and silver. Rafi replied: 'There is no harm in this. In the time of the Prophet, people rented land for the crops and straw that grew along the waterways. Sometimes there was a harvest, and sometimes there was none. People rented land this way, so the Prophet forbade it. As for rent that is fixed and guaranteed, there is no harm.'

— Sunan Ibn Majah

This hadith shows that it is forbidden to pre-arrange any geography, time, or quantity for land rented to tenant farmers. Jurists concluded that because of uncertainty, predetermined compensation for either party is not allowed. This ruling on tenant farming applies to other partnerships, including profit-sharing partnerships (mudaraba). Therefore, Ibn Qudamah believed that jurists reached a consensus that it is not allowed to pre-specify profits in a mudaraba.

Dr. Abdullah Al-Najjar wrote a detailed discussion on this hadith and the conclusions drawn from it. He argued that the prohibition does not stem from the condition of pre-specifying profit itself, but from the uncertainty (gharar) that could lead to disputes (citing the narrative and analysis in Al-Shawkani's Nayl Al-Awtar). On the other hand, he argued that this type of partnership is essentially an employment contract with an unknown reward, and is therefore full of uncertainty. However, a consensus ruling actually permits this contract (including profit sharing) despite the uncertainty (as Ibn Qudamah stated). Therefore, this type of partnership belongs to a category of contracts where uncertainty (including that caused by pre-specifying profit) is ignored, as long as it does not lead to legal disputes.

Dr. Al-Najjar presented many other arguments based on the analysis of Al-Shawkani and Ibn Qudamah. He said: This might be Rafi's own non-binding conclusion; it might be limited to specific types of tenant farming; Zayd ibn Thabit disagreed with this hadith, claiming it related to a specific incident where one person killed another (recorded by Abu Dawud); the hadith narrated by Ibn Umar suggests that renting land is permitted (recorded by Bukhari), which challenges the hadith; other companions of the Prophet, including Ibn Abbas and others, disagreed with Rafi's view. Ibn Qudamah said that some of Rafi's narrations differ from the consensus of the companions and must therefore be discarded.

At the Al-Azhar conference, Dr. Muhammad Rif'at Uthman presented a counter-argument. According to Al-Nawawi, the hadith does not forbid renting land for a fixed rent (which was the focus of previous arguments), but it does forbid pre-specifying profits.

Most jurists believe that a profit-sharing partnership (mudāraba) that is known to be flawed or invalid from the start is not allowed. Dr. Tantāwī focuses on the consensus view that when a mudāraba is considered flawed, such as when an investor's profit is specified in advance, the contract becomes an employment contract ('ijara). Under this, the entrepreneur or worker is entitled to a market wage, as noted by ibn al-Humām in Fath Al-Qadīr and Al-Shaficī in 'um. He summarizes this (2001, p. 133):

Therefore, we say that a bank investing for a pre-specified profit becomes an employee of the investor. The investor accepts the amount the bank gives them as their profit, and any excess profit, whatever it may be, is treated as the bank's wage. Thus, this type of transaction is free of interest (Ribā). In short, we cannot find any canonical text or convincing analogy that forbids specifying profit in advance as long as both parties agree.

Quotes from early jurists

Dr. Tantāwī (2001, p. 95) quotes Dr. Khallāf, who in turn quotes Muhammad Abduh's 1906 article in Manār (#9, p. 332): When a person gives their money to another for investment and receives a known profit, this does not constitute clearly forbidden Ribā, regardless of the pre-specified profit rate. This is because legal rules that disagree on forbidding pre-specified profit do not constitute the clear type of Ribā that ruins families. This type of transaction is beneficial to both the investor and the entrepreneur. In contrast, Ribā for the borrower is only due to need and is not their fault, while for the lender, Ribā leads to greed and a hardened heart. These two types of transactions cannot have the same legal status (hukm).

Dr. Khallāf, in Liwā' 'Islām (1951, #4 (11)), continues (quoted in the same, pp. 95-6): There is no evidence that profit cannot be specified in advance. Just as profit can be shared between two parties, the profit for one party can also be specified in advance. Such a condition might not align with the views of jurists, but it does not contradict any canonical text in the Quran or Sunnah.

Core argument

Dr. Khallaf summarizes the basis for the current Al-Azhar ruling as follows: The only objection to this type of transaction is the validity of mudāraba, which requires that profit must be set as a percentage share rather than a specific capital amount or percentage. My response to this objection is as follows: First, there is no evidence for this condition in the Quran or the Sunnah. We live in a very dishonest time now, and if we do not set a fixed profit for the investor, his partner will swallow up his wealth.

Second, if a mudāraba is considered flawed because it violates one of its conditions, the entrepreneur becomes an employee, and what he takes is considered a wage. There is no difference in calling it mudāraba or 'ijāra: it is a valid transaction that benefits the investor who cannot invest funds directly and benefits the entrepreneur who receives the funds. Therefore, this is a transaction that benefits both parties without harming either side or anyone else, and banning such a beneficial transaction will harm the Ummah.

Key points

Recent academic journals from Al-Azhar do allow certain types of bank interest to be used as investment profit.

This fatwa is at least a century old.

Most jurists oppose this fatwa.

A minority have questioned the authenticity, authority, and applicability of the hadith regarding sharecroppers.

A minority have questioned the logic of prohibiting the pre-specification of profit.

Can we still claim that a consensus exists?

If this issue is controversial, should we proceed with caution? Should we follow the view of the majority?

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.

This set profit rate can go up or down over time. For example, an investment project might start with a 4% return, grow to over 15%, and then recently drop back to near 10%.

The people who set these rates and manage their changes must follow government rules. Setting a fixed number in advance—especially in these times when honesty is rare—benefits both the investors and the bank.

Investors benefit from stable profit rates, which helps them plan their lives. Bank managers benefit from performance incentives, which push them to work harder to maximize profits and keep the bank profitable even after paying the investors their set returns. What if the bank loses money during that time? How can it set a profit rate in advance? The answer is that a bank might lose money on one investment but make a profit on many others, which covers the loss.

In short: it is allowed for someone to invest money through an institution into a bank or other financial firm with a pre-set profit. There is nothing suspicious about it. This type of transaction is judged by its benefits and is not considered associating partners with Allah (shirk). Therefore, investing money in a bank with a pre-agreed profit or return is allowed and causes no harm. Allah knows best.

What does this religious ruling (fatwa) not say?

Please note that this fatwa does not explicitly state that all bank interest is halal.

Dr. Tantawi has clearly stated elsewhere that interest on bank deposits is riba, and interest on bank loans is also riba. (See Mucamalat al-Bunuk..., 2001, pp. 139-142)

There are three points of contention here.

First, are funds held for business operations considered deposits?

Second, are funds borrowed for business operations considered loans?

Third, is it forbidden to pre-determine the profit for one party in an investment activity?

There is little disagreement regarding deposits.

There is substantial disagreement regarding loans:

Abdullah Al-Najjar explains Dr. Tantawi's position as follows:

Funds given to a bank cannot be seen as a form of loan because the bank has no need, and only those in need apply for loans. Anas ibn Malik reported that the Prophet said: 'On the night of the Ascension, I saw written on the gate of Paradise: Charity is rewarded tenfold, and a loan is rewarded eighteenfold.' I said: 'O Jibril!' Why is borrowing more expensive than giving charity? The angel Jibril said: 'Because a beggar asks when they still have something, but a borrower only asks when they are in urgent need.' — Sunan Ibn Majah

Therefore, if a transaction is not a loan, bank customers must be seen as investors who intend to seek profit from the bank (the bank announces the return rate they pay, and customers choose the bank they prefer).

Jurists believe that once deposit funds are used, they are promised, and because holding a guarantee (like a loan) is more reliable than holding a trust (like a deposit), the deposit contract becomes a loan, and any increase is forbidden interest (riba).

the 'preset profit' in profit-sharing (mudaraba) is the core of what this Islamic law forbids.

Al-Qaradawi and many others believe that the hadith regarding sharecropping (muzara'ah) provides the basis for the prohibition. The Sharia committee mentioned the claim of 'consensus' put forward by Ibn Qudamah in Al-Mughni and confirmed that this 'consensus' is as binding as the classical texts.

The 14th session of the Fiqh Academy, January 2003, Decision #133 (7/14), pages 20-24.

Religious law and secular law describe the relationship between a depositor and a bank as a loan relationship, not an agency relationship. In contrast, an investment agency is where an agent invests funds on behalf of a principal in exchange for a fixed wage or a share of the profits. In this regard, religious scholars have a consensus that the principal owns the investment funds and therefore has the right to receive investment gains and is responsible for losses, while the agent has the right to receive a fixed wage under the conditions set by the agency. Therefore, a traditional bank is not an investment agent for the depositor. The bank receives funds from the depositor and uses them, thereby guaranteeing said funds and making them a loan. In this regard, the loan must be repaid at face value without any increase.

For centuries, jurists from all schools have agreed that you cannot pre-set investment profits in any partnership, whether as a fixed amount or a percentage of the capital. This ruling is based on the idea that pre-setting profits guarantees the principal, which goes against the nature of a partnership where you must share both profits and losses. This consensus is well-established and has no reported disagreements. In this regard, Ibn Qudamah wrote in Al-Mughni (Volume 3, page 34): All scholars agree that if one or both parties set a known amount of profit, the partnership (qirad or mudaraba) becomes invalid. The consensus of religious scholars is itself a legal proof.

Pre-specifying profits

Dr. Tantawi and his supporters rejected the loan issue and held a long discussion on the problem of pre-set profits. Dr. Tantawi cited Abdul-Wahhab Khallaf and Dr. Ali Al-Khafif to support his view that it is inappropriate to limit investment institutions to traditional mudaraba, which has profit sharing but no specific profit amount.

The main argument for fixed profits

Tantawi (2001, page 131) quoted Khallaf (pages 94-104), Al-Khafif (pages 165-204), and others (pages 204-211) word for word, saying: In this era of corruption, dishonesty, and greed, not fixing profits as a percentage of capital would leave the principal at the mercy of the agents managing the investment funds, whether they are banks or other institutions.

Therefore, he and earlier scholars turned to the well-known issue of moral hazard, which is unrelated to profit distribution.

Second, once the loan or deposit argument is rejected, the remaining issue is how to handle the consensus theory in Al-Mughni and the hadith it is based on.

Is the claim of consensus accepted? Is it binding?

Does this decision have a basis in the Quran and Sunnah, or can it be overturned?

If a partnership is considered flawed because the profit margin is predetermined, does this make it forbidden interest (riba), or is it a permitted lease (ijara), such as whether a mutually agreed upon (though uncertain) wage payment is legal?

Hadith on tenant farming.

Hanzalah ibn Qays narrated: I asked Rafi ibn Khadij about renting land for gold and silver. Rafi replied: 'There is no harm in this. In the time of the Prophet, people rented land for the crops and straw that grew along the waterways. Sometimes there was a harvest, and sometimes there was none. People rented land this way, so the Prophet forbade it. As for rent that is fixed and guaranteed, there is no harm.'

— Sunan Ibn Majah

This hadith shows that it is forbidden to pre-arrange any geography, time, or quantity for land rented to tenant farmers. Jurists concluded that because of uncertainty, predetermined compensation for either party is not allowed. This ruling on tenant farming applies to other partnerships, including profit-sharing partnerships (mudaraba). Therefore, Ibn Qudamah believed that jurists reached a consensus that it is not allowed to pre-specify profits in a mudaraba.

Dr. Abdullah Al-Najjar wrote a detailed discussion on this hadith and the conclusions drawn from it. He argued that the prohibition does not stem from the condition of pre-specifying profit itself, but from the uncertainty (gharar) that could lead to disputes (citing the narrative and analysis in Al-Shawkani's Nayl Al-Awtar). On the other hand, he argued that this type of partnership is essentially an employment contract with an unknown reward, and is therefore full of uncertainty. However, a consensus ruling actually permits this contract (including profit sharing) despite the uncertainty (as Ibn Qudamah stated). Therefore, this type of partnership belongs to a category of contracts where uncertainty (including that caused by pre-specifying profit) is ignored, as long as it does not lead to legal disputes.

Dr. Al-Najjar presented many other arguments based on the analysis of Al-Shawkani and Ibn Qudamah. He said: This might be Rafi's own non-binding conclusion; it might be limited to specific types of tenant farming; Zayd ibn Thabit disagreed with this hadith, claiming it related to a specific incident where one person killed another (recorded by Abu Dawud); the hadith narrated by Ibn Umar suggests that renting land is permitted (recorded by Bukhari), which challenges the hadith; other companions of the Prophet, including Ibn Abbas and others, disagreed with Rafi's view. Ibn Qudamah said that some of Rafi's narrations differ from the consensus of the companions and must therefore be discarded.

At the Al-Azhar conference, Dr. Muhammad Rif'at Uthman presented a counter-argument. According to Al-Nawawi, the hadith does not forbid renting land for a fixed rent (which was the focus of previous arguments), but it does forbid pre-specifying profits.

Most jurists believe that a profit-sharing partnership (mudāraba) that is known to be flawed or invalid from the start is not allowed. Dr. Tantāwī focuses on the consensus view that when a mudāraba is considered flawed, such as when an investor's profit is specified in advance, the contract becomes an employment contract ('ijara). Under this, the entrepreneur or worker is entitled to a market wage, as noted by ibn al-Humām in Fath Al-Qadīr and Al-Shaficī in 'um. He summarizes this (2001, p. 133):

Therefore, we say that a bank investing for a pre-specified profit becomes an employee of the investor. The investor accepts the amount the bank gives them as their profit, and any excess profit, whatever it may be, is treated as the bank's wage. Thus, this type of transaction is free of interest (Ribā). In short, we cannot find any canonical text or convincing analogy that forbids specifying profit in advance as long as both parties agree.

Quotes from early jurists

Dr. Tantāwī (2001, p. 95) quotes Dr. Khallāf, who in turn quotes Muhammad Abduh's 1906 article in Manār (#9, p. 332): When a person gives their money to another for investment and receives a known profit, this does not constitute clearly forbidden Ribā, regardless of the pre-specified profit rate. This is because legal rules that disagree on forbidding pre-specified profit do not constitute the clear type of Ribā that ruins families. This type of transaction is beneficial to both the investor and the entrepreneur. In contrast, Ribā for the borrower is only due to need and is not their fault, while for the lender, Ribā leads to greed and a hardened heart. These two types of transactions cannot have the same legal status (hukm).

Dr. Khallāf, in Liwā' 'Islām (1951, #4 (11)), continues (quoted in the same, pp. 95-6): There is no evidence that profit cannot be specified in advance. Just as profit can be shared between two parties, the profit for one party can also be specified in advance. Such a condition might not align with the views of jurists, but it does not contradict any canonical text in the Quran or Sunnah.

Core argument

Dr. Khallaf summarizes the basis for the current Al-Azhar ruling as follows: The only objection to this type of transaction is the validity of mudāraba, which requires that profit must be set as a percentage share rather than a specific capital amount or percentage. My response to this objection is as follows: First, there is no evidence for this condition in the Quran or the Sunnah. We live in a very dishonest time now, and if we do not set a fixed profit for the investor, his partner will swallow up his wealth.

Second, if a mudāraba is considered flawed because it violates one of its conditions, the entrepreneur becomes an employee, and what he takes is considered a wage. There is no difference in calling it mudāraba or 'ijāra: it is a valid transaction that benefits the investor who cannot invest funds directly and benefits the entrepreneur who receives the funds. Therefore, this is a transaction that benefits both parties without harming either side or anyone else, and banning such a beneficial transaction will harm the Ummah.

Key points

Recent academic journals from Al-Azhar do allow certain types of bank interest to be used as investment profit.

This fatwa is at least a century old.

Most jurists oppose this fatwa.

A minority have questioned the authenticity, authority, and applicability of the hadith regarding sharecroppers.

A minority have questioned the logic of prohibiting the pre-specification of profit.

Can we still claim that a consensus exists?

If this issue is controversial, should we proceed with caution? Should we follow the view of the majority?

Muslim Knowledge Guide Al-Azhar: Bank Interest, Riba Fatwa and Islamic Finance Debate

Articles • yusuf908 posted the article • 0 comments • 119 views • 2026-05-23 02:38

Reposted from the web

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.

This set profit rate can go up or down over time. For example, an investment project might start with a 4% return, grow to over 15%, and then recently drop back to near 10%.

The people who set these rates and manage their changes must follow government rules. Setting a fixed number in advance—especially in these times when honesty is rare—benefits both the investors and the bank.

Investors benefit from stable profit rates, which helps them plan their lives. Bank managers benefit from performance incentives, which push them to work harder to maximize profits and keep the bank profitable even after paying the investors their set returns. What if the bank loses money during that time? How can it set a profit rate in advance? The answer is that a bank might lose money on one investment but make a profit on many others, which covers the loss.

In short: it is allowed for someone to invest money through an institution into a bank or other financial firm with a pre-set profit. There is nothing suspicious about it. This type of transaction is judged by its benefits and is not considered associating partners with Allah (shirk). Therefore, investing money in a bank with a pre-agreed profit or return is allowed and causes no harm. Allah knows best.

What does this religious ruling (fatwa) not say?

Please note that this fatwa does not explicitly state that all bank interest is halal.

Dr. Tantawi has clearly stated elsewhere that interest on bank deposits is riba, and interest on bank loans is also riba. (See Mucamalat al-Bunuk..., 2001, pp. 139-142)

There are three points of contention here.

First, are funds held for business operations considered deposits?

Second, are funds borrowed for business operations considered loans?

Third, is it forbidden to pre-determine the profit for one party in an investment activity?

There is little disagreement regarding deposits.

There is substantial disagreement regarding loans:

Abdullah Al-Najjar explains Dr. Tantawi's position as follows:

Funds given to a bank cannot be seen as a form of loan because the bank has no need, and only those in need apply for loans. Anas ibn Malik reported that the Prophet said: 'On the night of the Ascension, I saw written on the gate of Paradise: Charity is rewarded tenfold, and a loan is rewarded eighteenfold.' I said: 'O Jibril!' Why is borrowing more expensive than giving charity? The angel Jibril said: 'Because a beggar asks when they still have something, but a borrower only asks when they are in urgent need.' — Sunan Ibn Majah

Therefore, if a transaction is not a loan, bank customers must be seen as investors who intend to seek profit from the bank (the bank announces the return rate they pay, and customers choose the bank they prefer).

Jurists believe that once deposit funds are used, they are promised, and because holding a guarantee (like a loan) is more reliable than holding a trust (like a deposit), the deposit contract becomes a loan, and any increase is forbidden interest (riba).

the 'preset profit' in profit-sharing (mudaraba) is the core of what this Islamic law forbids.

Al-Qaradawi and many others believe that the hadith regarding sharecropping (muzara'ah) provides the basis for the prohibition. The Sharia committee mentioned the claim of 'consensus' put forward by Ibn Qudamah in Al-Mughni and confirmed that this 'consensus' is as binding as the classical texts.

The 14th session of the Fiqh Academy, January 2003, Decision #133 (7/14), pages 20-24.

Religious law and secular law describe the relationship between a depositor and a bank as a loan relationship, not an agency relationship. In contrast, an investment agency is where an agent invests funds on behalf of a principal in exchange for a fixed wage or a share of the profits. In this regard, religious scholars have a consensus that the principal owns the investment funds and therefore has the right to receive investment gains and is responsible for losses, while the agent has the right to receive a fixed wage under the conditions set by the agency. Therefore, a traditional bank is not an investment agent for the depositor. The bank receives funds from the depositor and uses them, thereby guaranteeing said funds and making them a loan. In this regard, the loan must be repaid at face value without any increase.

For centuries, jurists from all schools have agreed that you cannot pre-set investment profits in any partnership, whether as a fixed amount or a percentage of the capital. This ruling is based on the idea that pre-setting profits guarantees the principal, which goes against the nature of a partnership where you must share both profits and losses. This consensus is well-established and has no reported disagreements. In this regard, Ibn Qudamah wrote in Al-Mughni (Volume 3, page 34): All scholars agree that if one or both parties set a known amount of profit, the partnership (qirad or mudaraba) becomes invalid. The consensus of religious scholars is itself a legal proof.

Pre-specifying profits

Dr. Tantawi and his supporters rejected the loan issue and held a long discussion on the problem of pre-set profits. Dr. Tantawi cited Abdul-Wahhab Khallaf and Dr. Ali Al-Khafif to support his view that it is inappropriate to limit investment institutions to traditional mudaraba, which has profit sharing but no specific profit amount.

The main argument for fixed profits

Tantawi (2001, page 131) quoted Khallaf (pages 94-104), Al-Khafif (pages 165-204), and others (pages 204-211) word for word, saying: In this era of corruption, dishonesty, and greed, not fixing profits as a percentage of capital would leave the principal at the mercy of the agents managing the investment funds, whether they are banks or other institutions.

Therefore, he and earlier scholars turned to the well-known issue of moral hazard, which is unrelated to profit distribution.

Second, once the loan or deposit argument is rejected, the remaining issue is how to handle the consensus theory in Al-Mughni and the hadith it is based on.

Is the claim of consensus accepted? Is it binding?

Does this decision have a basis in the Quran and Sunnah, or can it be overturned?

If a partnership is considered flawed because the profit margin is predetermined, does this make it forbidden interest (riba), or is it a permitted lease (ijara), such as whether a mutually agreed upon (though uncertain) wage payment is legal?

Hadith on tenant farming.

Hanzalah ibn Qays narrated: I asked Rafi ibn Khadij about renting land for gold and silver. Rafi replied: 'There is no harm in this. In the time of the Prophet, people rented land for the crops and straw that grew along the waterways. Sometimes there was a harvest, and sometimes there was none. People rented land this way, so the Prophet forbade it. As for rent that is fixed and guaranteed, there is no harm.'

— Sunan Ibn Majah

This hadith shows that it is forbidden to pre-arrange any geography, time, or quantity for land rented to tenant farmers. Jurists concluded that because of uncertainty, predetermined compensation for either party is not allowed. This ruling on tenant farming applies to other partnerships, including profit-sharing partnerships (mudaraba). Therefore, Ibn Qudamah believed that jurists reached a consensus that it is not allowed to pre-specify profits in a mudaraba.

Dr. Abdullah Al-Najjar wrote a detailed discussion on this hadith and the conclusions drawn from it. He argued that the prohibition does not stem from the condition of pre-specifying profit itself, but from the uncertainty (gharar) that could lead to disputes (citing the narrative and analysis in Al-Shawkani's Nayl Al-Awtar). On the other hand, he argued that this type of partnership is essentially an employment contract with an unknown reward, and is therefore full of uncertainty. However, a consensus ruling actually permits this contract (including profit sharing) despite the uncertainty (as Ibn Qudamah stated). Therefore, this type of partnership belongs to a category of contracts where uncertainty (including that caused by pre-specifying profit) is ignored, as long as it does not lead to legal disputes.

Dr. Al-Najjar presented many other arguments based on the analysis of Al-Shawkani and Ibn Qudamah. He said: This might be Rafi's own non-binding conclusion; it might be limited to specific types of tenant farming; Zayd ibn Thabit disagreed with this hadith, claiming it related to a specific incident where one person killed another (recorded by Abu Dawud); the hadith narrated by Ibn Umar suggests that renting land is permitted (recorded by Bukhari), which challenges the hadith; other companions of the Prophet, including Ibn Abbas and others, disagreed with Rafi's view. Ibn Qudamah said that some of Rafi's narrations differ from the consensus of the companions and must therefore be discarded.

At the Al-Azhar conference, Dr. Muhammad Rif'at Uthman presented a counter-argument. According to Al-Nawawi, the hadith does not forbid renting land for a fixed rent (which was the focus of previous arguments), but it does forbid pre-specifying profits.

Most jurists believe that a profit-sharing partnership (mudāraba) that is known to be flawed or invalid from the start is not allowed. Dr. Tantāwī focuses on the consensus view that when a mudāraba is considered flawed, such as when an investor's profit is specified in advance, the contract becomes an employment contract ('ijara). Under this, the entrepreneur or worker is entitled to a market wage, as noted by ibn al-Humām in Fath Al-Qadīr and Al-Shaficī in 'um. He summarizes this (2001, p. 133):

Therefore, we say that a bank investing for a pre-specified profit becomes an employee of the investor. The investor accepts the amount the bank gives them as their profit, and any excess profit, whatever it may be, is treated as the bank's wage. Thus, this type of transaction is free of interest (Ribā). In short, we cannot find any canonical text or convincing analogy that forbids specifying profit in advance as long as both parties agree.

Quotes from early jurists

Dr. Tantāwī (2001, p. 95) quotes Dr. Khallāf, who in turn quotes Muhammad Abduh's 1906 article in Manār (#9, p. 332): When a person gives their money to another for investment and receives a known profit, this does not constitute clearly forbidden Ribā, regardless of the pre-specified profit rate. This is because legal rules that disagree on forbidding pre-specified profit do not constitute the clear type of Ribā that ruins families. This type of transaction is beneficial to both the investor and the entrepreneur. In contrast, Ribā for the borrower is only due to need and is not their fault, while for the lender, Ribā leads to greed and a hardened heart. These two types of transactions cannot have the same legal status (hukm).

Dr. Khallāf, in Liwā' 'Islām (1951, #4 (11)), continues (quoted in the same, pp. 95-6): There is no evidence that profit cannot be specified in advance. Just as profit can be shared between two parties, the profit for one party can also be specified in advance. Such a condition might not align with the views of jurists, but it does not contradict any canonical text in the Quran or Sunnah.

Core argument

Dr. Khallaf summarizes the basis for the current Al-Azhar ruling as follows: The only objection to this type of transaction is the validity of mudāraba, which requires that profit must be set as a percentage share rather than a specific capital amount or percentage. My response to this objection is as follows: First, there is no evidence for this condition in the Quran or the Sunnah. We live in a very dishonest time now, and if we do not set a fixed profit for the investor, his partner will swallow up his wealth.

Second, if a mudāraba is considered flawed because it violates one of its conditions, the entrepreneur becomes an employee, and what he takes is considered a wage. There is no difference in calling it mudāraba or 'ijāra: it is a valid transaction that benefits the investor who cannot invest funds directly and benefits the entrepreneur who receives the funds. Therefore, this is a transaction that benefits both parties without harming either side or anyone else, and banning such a beneficial transaction will harm the Ummah.

Key points

Recent academic journals from Al-Azhar do allow certain types of bank interest to be used as investment profit.

This fatwa is at least a century old.

Most jurists oppose this fatwa.

A minority have questioned the authenticity, authority, and applicability of the hadith regarding sharecroppers.

A minority have questioned the logic of prohibiting the pre-specification of profit.

Can we still claim that a consensus exists?

If this issue is controversial, should we proceed with caution? Should we follow the view of the majority? view all

Summary: This Muslim knowledge guide translates and explains Mahmoud A. El-Gamal's discussion of an Al-Azhar fatwa on bank interest, fixed investment profits, riba, mudaraba, jurist disagreement, historical context, and whether bank returns can be treated as lawful investment income.

I posted a screenshot of a book written by Imam Chen Yufeng on my social media. At the end of the book, Imam Chen shares a personal experience regarding interest. He mentions that issue 168 of the Al-Azhar Journal once ruled bank interest as lawful. A friend later found the original source of this fatwa, along with a commentary article explaining the background of the ruling, titled

“The recent Azhar fatwā:Its logic, and historical background”

I will not post the link here, so please search for it yourself. The original text is in English and includes the Arabic version. I have translated the article below for your reference, as it complements the post I shared earlier.

You cannot buy Imam Chen's book, and there is no digital version, so please stop asking me how to purchase it.

“The recent Azhar fatwā:Its logic, and historical background”

Author: Mahmoud A. El-Gamal

Rice University, USA

Author's Preface:

I am not a jurist, but an academic researcher. Therefore, I am not qualified to endorse or reject this fatwa. The purpose of this article is only to explain and summarize the ruling. To explain what this fatwa says? It says nothing. How scholars view it and the logic behind it.

What does this religious ruling (fatwa) say?

It is perfectly fine to deposit your money in a bank and appoint the bank as your agent for investments in exchange for an agreed-upon profit. Neither the Quran nor the Hadith forbids this kind of deal where profit or payment is set in advance, as long as both sides agree to it.

There is no doubt that both sides agreeing to a set profit beforehand is allowed under Islamic law. It also makes logical sense so that each party knows exactly what their share will be.

As everyone knows, a bank only sets these profits or returns for clients after carefully studying global and local markets, economic conditions, the specifics of each deal, the type of investment, and the average expected profit.