Interest_Free Banking

Muslim Knowledge Guide China: Interest-Free Banking, Islamic Finance and Service Fee Debate

Articles • yusuf908 posted the article • 0 comments • 121 views • 2026-05-23 06:09

Reposted from the web

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

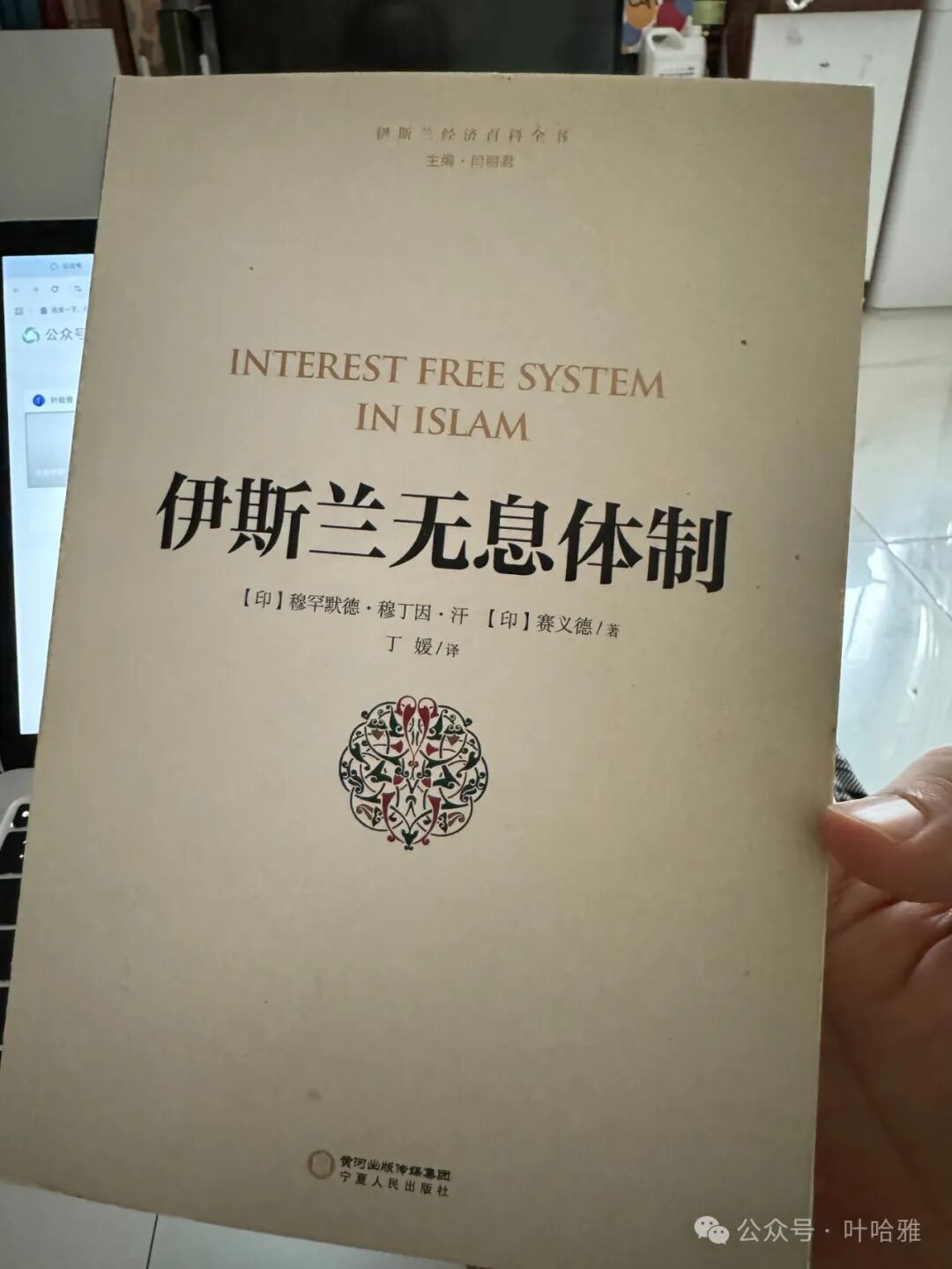

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue. view all

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue. view all

Reposted from the web

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue.

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue.

Muslim Knowledge Guide China: Interest-Free Banking, Islamic Finance and Service Fee Debate

Articles • yusuf908 posted the article • 0 comments • 121 views • 2026-05-23 06:09

Reposted from the web

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue. view all

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue. view all

Reposted from the web

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue.

Summary: This Muslim knowledge guide reviews an interest-free banking book, compares service fees with riba, discusses Islamic finance, dividend insurance, IUL, gold investment, mutual aid systems, and the practical challenge of building an interest-free bank in modern society.

This book is a formal publication available on Taobao. While its main goal is to explain the interest-free financial system proposed by the authors, they are honest enough to mention that such a system does not yet exist in today's society. However, perhaps because the book has two authors, it feels inconsistent throughout. Here are some of my reading notes.

Author 1, Muhammad Muin-ud-Din Khan, graduated from Aligarh Muslim University with a Bachelor of Laws and a Master of Arts. He currently lives in Aligarh and works on Islamic law research.

Author 2, M. H. Syed, is a feature writer for the United Times of India and the Times of India. He holds a Master of Arts, a Master of Philosophy, and a PhD in political science, and he focuses mainly on political research with a wide range of interests.

In the second chapter, when citing examples from Christianity, the authors criticize the way Christians confuse service fees with interest:

With the support of Christian churches, the practice of using service fees to replace interest developed further. At first, following the precedents of ancient Babylonian and ancient Greek temples, they provided interest-free loans. Soon, people found it necessary to charge a small fee for services. Lending institutions that charged service fees were called Montes Pietatis. Before long, these institutions were no different from savings banks. They paid small amounts of interest on deposits and charged high interest on advances, which shows that replacing the concept of interest with this idea is very unreliable. Important concepts that evolved under Christian influence, such as tripartite contracts and perpetual annuities, are also much the same as interest.

However, in the second half of the book, the author proposes an interest-free bank and acknowledges the necessity of service fees. As my previous articles have noted, critics of Islamic finance point out that charging service fees in an interest-free bank is just a way to legalize interest in disguise.

The author also imagines an interest-free bank as a financial institution that protects the principal but offers uncertain returns. This confused me because such institutions already exist. In China, these are called dividend-paying insurance (fenhongxing baoxian), and in the United States, they are called Indexed Universal Life (IUL) insurance. Both types protect the principal but have uncertain future returns. Dividend insurance dates back to the Equitable Life Assurance Society in the UK in 1776, and IUL insurance began in the US in the 1990s.

The author honestly describes the current situation where both Jews and Muslims find themselves helpless regarding the issue of interest:

The role of the Jews: The first interest-free bank, the Egibi Bank, was opened by Jews in ancient Babylon in 700 BC. This bank used a method where borrowers pledged productive assets, such as houses, land, horses, or slaves, to the bank in exchange for interest-free loans. Although the concept of profit and loss sharing was refined, the lack of productive assets limited its application. For example, profit and loss sharing cannot solve the problem of making installment prices equal to cash prices, nor can it solve the issue of cashing bills of exchange without deducting a discount. According to the famous Jewish scholar Maimonides, Jews also faced the difficult problem of how to cash bills of exchange. They solved it by declaring that discounts did not count as interest. This means that even financial geniuses like the Jews could not find a proper way to eliminate interest.

The role of Muslims: Muslims have not found a substitute for interest. Their reliance on partnerships is no different from the profit and loss sharing mechanism created by Hammurabi or the pre-Islamic mudarabah system—neither can be widely applied in most economic practices. They tried hard to find reward-based funding and invented various disguised terms as the basis for Pakistani banking operations, such as fair trade or perfect trade, but these functioned much like interest. It is no wonder why the London-based weekly The Economist calls it an Islamic-style lie. Post-revolutionary Iran, like some other countries that claim to have introduced Islamic banking systems, is playing the same game of pretense. Dr. El-Naggar conducted a small-scale innovative experiment in Egypt by founding the Mit Ghamr Savings Bank based on profit and loss sharing, hoping to attract small savings and support small-scale productive investments. However, its scope of application is very limited, and it requires subsidies to continue operating; if the subsidies stop, the bank would have to close.

Practice has proven that forcibly suppressing interest rates does not work. The lesson we learned from medieval European usury laws is that forcibly suppressing or lowering interest rates only leads to the emergence of a black market for high-interest loans. We have only one choice, which is to find something that can replace interest without having the exploitative nature of interest. Many existing views stem from the profit and loss sharing mechanism in the Code of Hammurabi, and Jews, Christians, and Muslims have all applied this view in turn, but they have all found its feasibility to be limited. So far, a view that can avoid this flaw has not yet been born.

The author is also very clear that none of the Islamic banks operating in the world today are based on interest-free principles:

Any investment bank operating in an Islamic country can advance funds to solvent enterprises on the basis of mudarabah or partnership. However, if the funds are not yet due, no bank will cash them out at their face value. The tragedy is that even though everyone acknowledges the Islamic ban on interest, not a single Muslim bank operates on an interest-free basis. In fact, no one knows how to implement the ban on interest, and when the government puts on pressure, they just find excuses and pretexts to brush it off. However, the Islamic ban on interest is unlikely to end like previous religious policies, because government pressure will not weaken; it will only get stronger.

Both authors are Indian, but they use Pakistan as their research subject. The book also introduces the attitudes of some Pakistani officials toward interest:

In 1981, an international monetary and fiscal conference was held in Islamabad, the capital of Pakistan, and Islamic economists were the main participants. They proposed renaming interest, which was equivalent to abolishing it. The worst part was that everyone agreed to this arrangement without reservation, because it was the best suggestion they could come up with so far.

The late Auditor General of Pakistan set a good example for us. He spent most of his retirement trying to legalize the interest on his welfare fund savings, wanting to prove that Islam does not ban interest, and he even wrote a book to explain this view.

The authors used these two examples critically, but I read the opposite meaning from them. This also echoes Mohammad Omar Farooq's question: Is it a consensus that usury is the same as interest? This article, titled 'Is Interest the Same as Riba Mentioned in the Quran?', shows that there is still no consensus on this issue.