Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices

Reposted from the web

Summary: Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices is presented here as a clear English account for Muslim readers, beginning with this scene: There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever. The article keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Islamic Insurance, Takaful, Muslim Finance.

Islamic finance books that can be sold publicly in mainland China.

There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever judges incorrectly must bear the consequences.

Currently, scholars have three views on insurance. The first considers insurance haram (forbidden), the second considers it lawful, and the third is a middle ground, suggesting the insurance system needs reform to remove its unlawful parts.

Scholars who view insurance as unlawful argue that it contains elements of interest and gambling. They believe insurance involves interest because life insurance contracts promise a fixed payout at a set time, which carries the suspicion of interest. Health insurance contracts are uncertain about when a payout will occur, as it only happens if the client faces a loss, and this uncertainty carries the suspicion of gambling.

It is undeniable that interest and gambling are explicitly forbidden in the Quran. The Quran mentions the prohibition of interest four times: Surah Ar-Rum verse 39, Surah An-Nisa verse 161, Surah Al-Imran verses 130-132, and Surah Al-Baqarah verses 275-281.

Whatever you give for interest to increase within the wealth of people will not increase with Allah. But what you give in charity, desiring the countenance of Allah—those are the multipliers. (Surah Ar-Rum, verse 39)

The schools of jurisprudence have slight differences regarding interest. For example, regarding interest on debt, all four major schools agree that any loan that brings a benefit involves interest. However, Ibn Hazm mentions in his book Al-Muhalla that interest is not allowed in sales or deferred payments, except for six items: gold, silver, wheat, barley, dates, and salt. But for loans, interest is allowed for any commodity. The basis for this is a Hadith narrated by Abu Hurairah: The best among you is the one who is best in repayment. However, there are different opinions regarding this Hadith, as other Hadiths mention: Gold for gold, silver for silver.

Regarding the views of the four major schools of jurisprudence on interest, I will only cite their views on the exchange of goods that cannot be calculated, measured, or weighed:

1. Hanafi school: Profit is allowed in both spot transactions and deferred transactions.

2. Shafi'i school: Profit is allowed in both spot transactions and deferred transactions.

3. Maliki school: Deferred transactions are not allowed even without profit, but profit is allowed in spot transactions.

4. Hanbali school: Profit is allowed in both spot transactions and deferred transactions.

Imam Abu Hanifa, the founder of the Hanafi school, allowed Muslims to enter non-Muslim territories and trade based on interest. He also allowed Muslims to trade on a similar interest-based model with people who converted to Islam from non-Islamic countries. This means that for Muslims, receiving interest is illegal, but paying interest is not. However, the Shafi'i, Maliki, and Hanbali schools all disagree with the Hanafi view.

I am quoting the views of scholars not to prove that interest is legal. On the contrary, I firmly believe that interest is

illegal, no matter what form it takes. I just find that in modern society, it is impossible for us to avoid getting the dust of interest on us. As long as we use banks in our daily lives, we will inevitably have a relationship with interest. Even the companies we work for pay our salaries through banks, and the company's operating income deposited in banks will inevitably generate interest. If we want to completely cut off interest, we can only isolate ourselves from the world.

Ibn Mas'ud narrated that the Prophet said: 'Before the Day of Judgment, interest will be widespread.' 'Signs of the End Times' by Yusuf al-Wabil. Al-Mundhiri considered the narrators of this hadith to be reliable.

Abu Hurairah narrated that the Messenger of Allah said: 'A time will come when everyone will consume interest. Even if someone does not consume it, they will still be touched by the dust of interest.' 'Sunan Abu Dawood', Hadith 3331.

Such days have already arrived. The social pension insurance that the state mandates can be seen as an extension of interest, as we receive monthly payments after retirement. Who living in a city can avoid this? If we do not rely on pension insurance, how will we live when we get old? We can only rely on our children for support, but how can we guarantee our children's future lives? Besides, there are also elderly people who have no children.

Let's discuss another controversy in insurance: is buying insurance equivalent to gambling?

They ask you about the ruling on wine and gambling. Say: 'In both there is great sin, and some benefit for people, but the sin of them is greater than their benefit.' (Surah Al-Baqarah, verse 219)

Gambling is illegal in most countries, and Islam is no exception. Some scholars argue that gambling is forbidden because of uncertainty, but everyone knows gambling ruins families and encourages people to get something for nothing. People gamble to make a profit without putting in real work, which feeds human greed. This is the real reason Islam forbids it, not just because of uncertainty. Strictly speaking, gambling results are not truly uncertain; they are just too complex for the average person to predict, though they can be calculated with advanced technology.

Insurance contracts clearly state when a claim can be made and for how long the policy lasts. This provides a service of protection. Even if we do not know when a risk will happen, the protection is always there. It is like paying for a bodyguard who only steps in when you are in danger. Does the fact that we do not know when danger will strike mean hiring a bodyguard is the same as gambling?

Buying insurance does not make a person go bankrupt. Insurance companies usually do not accept applications for coverage that exceeds a person's assets. They check the applicant's qualifications first. This is fundamentally different from gambling, which allows anyone to participate without restrictions. It is very hard to make a profit from insurance. When a risk event happens, it usually comes with the cost of a person's health or life. Intentionally committing insurance fraud is illegal, which is another fundamental difference between insurance and gambling.

Think about the rules against alcohol. Islam forbids alcohol because getting drunk makes people lose their reason and affects things like namaz. This leads to the ruling that anything that intoxicates is forbidden. Things that cause intoxication include alcohol in food and other narcotics. Ancient people did not know about chemical alcohol. When the alcohol content in a drink reaches a certain level, it makes you drunk. But chemistry students know that almost all fruit contains alcohol, and the riper the fruit, the higher the content. It is almost impossible to strictly forbid any trace of alcohol in food. That is why international halal food standards allow for tiny amounts of alcohol. I have discussed this in my article about non-halal foods mentioned in the scriptures. Already written.

So, the uncertainty in insurance is like the tiny amount of alcohol in food. It is hard to avoid and does not need to be avoided. We face many uncertain things in life. Uncertainty is not wrong as long as it does not harm anyone.

I also want to live in a place that is entirely lawful and away from controversial things. But think about it: for an average family, if they do not buy insurance, what better way is there to help them get through a crisis when a risk occurs? Should they ask for charity (niyat) in person or use online crowdfunding? Both are forms of begging, which the Hadith repeatedly discourages. I have written an article about the scriptures regarding begging, which you can read in my piece about being a Muslim who never begs, just like the Kazakh people.

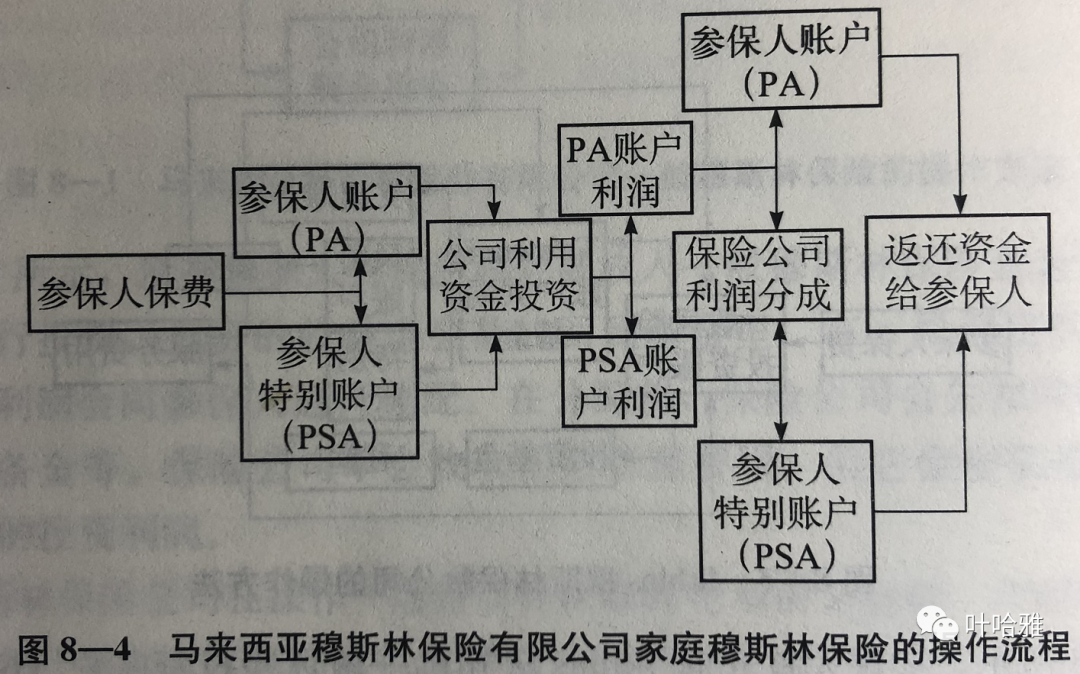

Finally, let us look at how Muslim insurance companies work. All Muslim insurance operators in Malaysia provide Muslim insurance services. If you buy a policy there, the contract requires you to pay a premium and also contribute a portion of money as a donation to help others hit by disaster. All premiums are put into a Muslim insurance fund. The company invests this money, and the profits go back into the fund. When the policy matures, the profits are distributed to the policyholders, and the insurance company deducts its fees to make a profit.

Screenshot from Islamic Banking and Financial Systems.

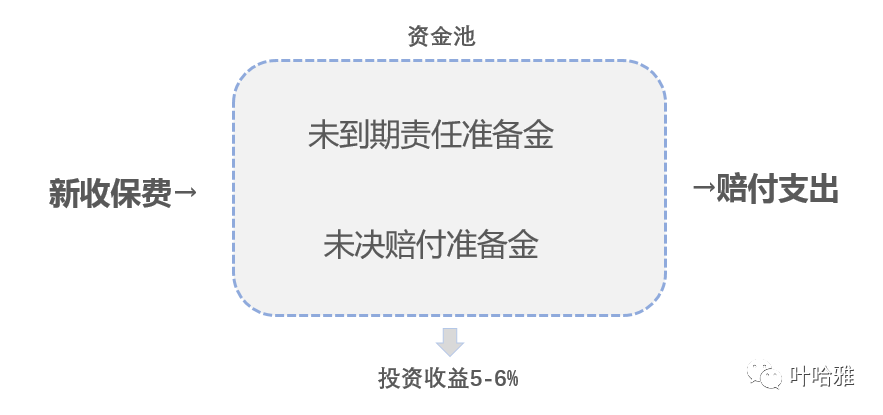

The way these Muslim insurance companies work is basically the same as the insurance companies in our country. The only difference is that Muslim insurance companies divide the premiums into different categories, and they do not invest in non-halal projects like alcohol. But from the customer's experience, both involve paying a premium to get protection. In this sense, the principle is the same for both types of insurance.

Capital flow of traditional insurance companies.

We can see that traditional insurance companies also split premiums into two parts after collecting them. One part is used as a reserve for emergencies, and the other is invested. The difference is that they are not Muslim insurance companies, so they are not restricted in where they can invest.

That is all I can think of for now regarding Islamic insurance. I hope my article helps clear up your questions. I am not trying to convince everyone. If you do not agree with insurance, you can just take responsibility for your own risks. Everyone should be responsible for their own actions. If you are interested in this, you can look at my previous posts about Islamic insurance and my career.

Summary: Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices is presented here as a clear English account for Muslim readers, beginning with this scene: There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever. The article keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Islamic Insurance, Takaful, Muslim Finance.

Islamic finance books that can be sold publicly in mainland China.

There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever judges incorrectly must bear the consequences.

Currently, scholars have three views on insurance. The first considers insurance haram (forbidden), the second considers it lawful, and the third is a middle ground, suggesting the insurance system needs reform to remove its unlawful parts.

Scholars who view insurance as unlawful argue that it contains elements of interest and gambling. They believe insurance involves interest because life insurance contracts promise a fixed payout at a set time, which carries the suspicion of interest. Health insurance contracts are uncertain about when a payout will occur, as it only happens if the client faces a loss, and this uncertainty carries the suspicion of gambling.

It is undeniable that interest and gambling are explicitly forbidden in the Quran. The Quran mentions the prohibition of interest four times: Surah Ar-Rum verse 39, Surah An-Nisa verse 161, Surah Al-Imran verses 130-132, and Surah Al-Baqarah verses 275-281.

Whatever you give for interest to increase within the wealth of people will not increase with Allah. But what you give in charity, desiring the countenance of Allah—those are the multipliers. (Surah Ar-Rum, verse 39)

The schools of jurisprudence have slight differences regarding interest. For example, regarding interest on debt, all four major schools agree that any loan that brings a benefit involves interest. However, Ibn Hazm mentions in his book Al-Muhalla that interest is not allowed in sales or deferred payments, except for six items: gold, silver, wheat, barley, dates, and salt. But for loans, interest is allowed for any commodity. The basis for this is a Hadith narrated by Abu Hurairah: The best among you is the one who is best in repayment. However, there are different opinions regarding this Hadith, as other Hadiths mention: Gold for gold, silver for silver.

Regarding the views of the four major schools of jurisprudence on interest, I will only cite their views on the exchange of goods that cannot be calculated, measured, or weighed:

1. Hanafi school: Profit is allowed in both spot transactions and deferred transactions.

2. Shafi'i school: Profit is allowed in both spot transactions and deferred transactions.

3. Maliki school: Deferred transactions are not allowed even without profit, but profit is allowed in spot transactions.

4. Hanbali school: Profit is allowed in both spot transactions and deferred transactions.

Imam Abu Hanifa, the founder of the Hanafi school, allowed Muslims to enter non-Muslim territories and trade based on interest. He also allowed Muslims to trade on a similar interest-based model with people who converted to Islam from non-Islamic countries. This means that for Muslims, receiving interest is illegal, but paying interest is not. However, the Shafi'i, Maliki, and Hanbali schools all disagree with the Hanafi view.

I am quoting the views of scholars not to prove that interest is legal. On the contrary, I firmly believe that interest is

illegal, no matter what form it takes. I just find that in modern society, it is impossible for us to avoid getting the dust of interest on us. As long as we use banks in our daily lives, we will inevitably have a relationship with interest. Even the companies we work for pay our salaries through banks, and the company's operating income deposited in banks will inevitably generate interest. If we want to completely cut off interest, we can only isolate ourselves from the world.

Ibn Mas'ud narrated that the Prophet said: 'Before the Day of Judgment, interest will be widespread.' 'Signs of the End Times' by Yusuf al-Wabil. Al-Mundhiri considered the narrators of this hadith to be reliable.

Abu Hurairah narrated that the Messenger of Allah said: 'A time will come when everyone will consume interest. Even if someone does not consume it, they will still be touched by the dust of interest.' 'Sunan Abu Dawood', Hadith 3331.

Such days have already arrived. The social pension insurance that the state mandates can be seen as an extension of interest, as we receive monthly payments after retirement. Who living in a city can avoid this? If we do not rely on pension insurance, how will we live when we get old? We can only rely on our children for support, but how can we guarantee our children's future lives? Besides, there are also elderly people who have no children.

Let's discuss another controversy in insurance: is buying insurance equivalent to gambling?

They ask you about the ruling on wine and gambling. Say: 'In both there is great sin, and some benefit for people, but the sin of them is greater than their benefit.' (Surah Al-Baqarah, verse 219)

Gambling is illegal in most countries, and Islam is no exception. Some scholars argue that gambling is forbidden because of uncertainty, but everyone knows gambling ruins families and encourages people to get something for nothing. People gamble to make a profit without putting in real work, which feeds human greed. This is the real reason Islam forbids it, not just because of uncertainty. Strictly speaking, gambling results are not truly uncertain; they are just too complex for the average person to predict, though they can be calculated with advanced technology.

Insurance contracts clearly state when a claim can be made and for how long the policy lasts. This provides a service of protection. Even if we do not know when a risk will happen, the protection is always there. It is like paying for a bodyguard who only steps in when you are in danger. Does the fact that we do not know when danger will strike mean hiring a bodyguard is the same as gambling?

Buying insurance does not make a person go bankrupt. Insurance companies usually do not accept applications for coverage that exceeds a person's assets. They check the applicant's qualifications first. This is fundamentally different from gambling, which allows anyone to participate without restrictions. It is very hard to make a profit from insurance. When a risk event happens, it usually comes with the cost of a person's health or life. Intentionally committing insurance fraud is illegal, which is another fundamental difference between insurance and gambling.

Think about the rules against alcohol. Islam forbids alcohol because getting drunk makes people lose their reason and affects things like namaz. This leads to the ruling that anything that intoxicates is forbidden. Things that cause intoxication include alcohol in food and other narcotics. Ancient people did not know about chemical alcohol. When the alcohol content in a drink reaches a certain level, it makes you drunk. But chemistry students know that almost all fruit contains alcohol, and the riper the fruit, the higher the content. It is almost impossible to strictly forbid any trace of alcohol in food. That is why international halal food standards allow for tiny amounts of alcohol. I have discussed this in my article about non-halal foods mentioned in the scriptures. Already written.

So, the uncertainty in insurance is like the tiny amount of alcohol in food. It is hard to avoid and does not need to be avoided. We face many uncertain things in life. Uncertainty is not wrong as long as it does not harm anyone.

I also want to live in a place that is entirely lawful and away from controversial things. But think about it: for an average family, if they do not buy insurance, what better way is there to help them get through a crisis when a risk occurs? Should they ask for charity (niyat) in person or use online crowdfunding? Both are forms of begging, which the Hadith repeatedly discourages. I have written an article about the scriptures regarding begging, which you can read in my piece about being a Muslim who never begs, just like the Kazakh people.

Finally, let us look at how Muslim insurance companies work. All Muslim insurance operators in Malaysia provide Muslim insurance services. If you buy a policy there, the contract requires you to pay a premium and also contribute a portion of money as a donation to help others hit by disaster. All premiums are put into a Muslim insurance fund. The company invests this money, and the profits go back into the fund. When the policy matures, the profits are distributed to the policyholders, and the insurance company deducts its fees to make a profit.

Screenshot from Islamic Banking and Financial Systems.

The way these Muslim insurance companies work is basically the same as the insurance companies in our country. The only difference is that Muslim insurance companies divide the premiums into different categories, and they do not invest in non-halal projects like alcohol. But from the customer's experience, both involve paying a premium to get protection. In this sense, the principle is the same for both types of insurance.

Capital flow of traditional insurance companies.

We can see that traditional insurance companies also split premiums into two parts after collecting them. One part is used as a reserve for emergencies, and the other is invested. The difference is that they are not Muslim insurance companies, so they are not restricted in where they can invest.

That is all I can think of for now regarding Islamic insurance. I hope my article helps clear up your questions. I am not trying to convince everyone. If you do not agree with insurance, you can just take responsibility for your own risks. Everyone should be responsible for their own actions. If you are interested in this, you can look at my previous posts about Islamic insurance and my career.