Islamic Insurance

Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance

Articles • yusuf908 posted the article • 0 comments • 61 views • 2026-05-24 00:17

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

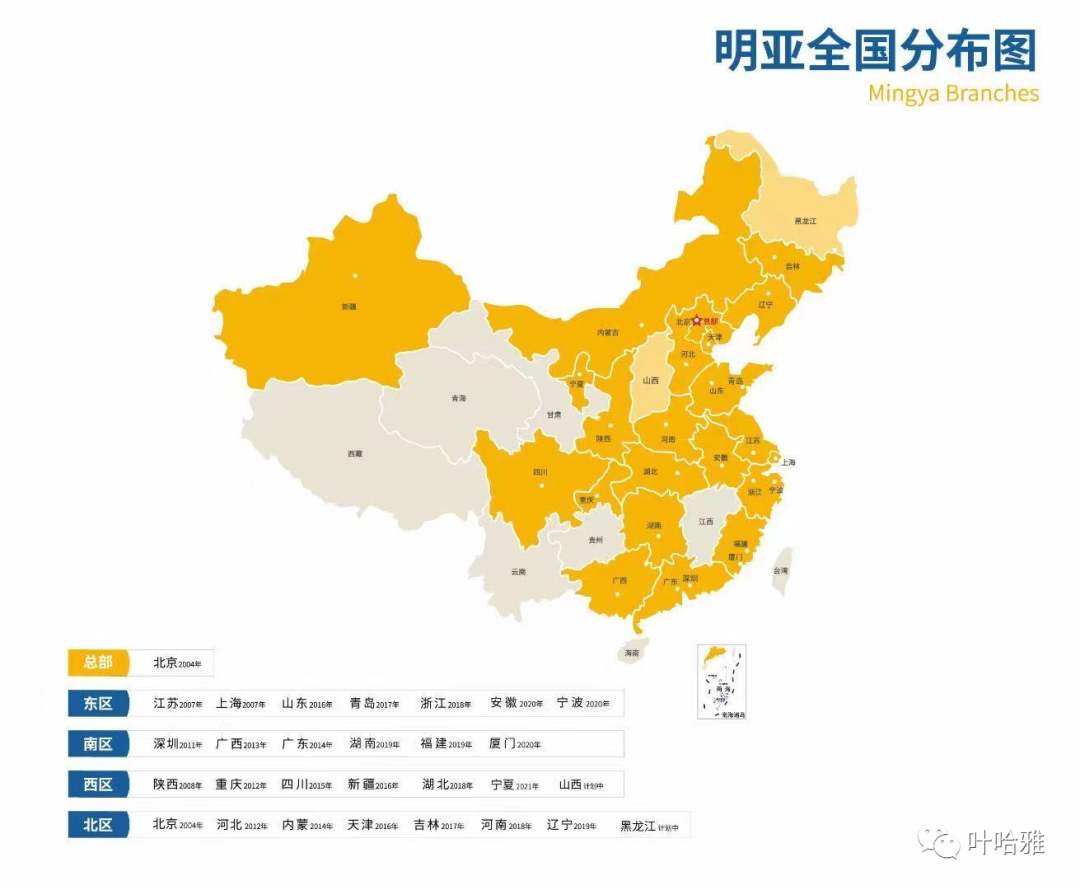

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.

Insurance brokers need high personal standards. People who cannot think for themselves or learn quickly are not suited for this job. The 80/20 rule applies here, but our situation is a bit better. About half of the people who join stay in the industry for at least a year. Please learn more about the job before you contact me. Please read the two articles I posted earlier for details on the job duties and requirements.

1. Islamic insurance and my career

2. Salaam, what can I do for you?

The regions listed above are provinces where we have branch offices. If you live in these areas, you can contact me for an interview and assessment. If you are in a place where we do not have a branch yet, do not worry. Our company will open new offices throughout the year. Tibet might be the only province-level area without a branch by the end. view all

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.

Insurance brokers need high personal standards. People who cannot think for themselves or learn quickly are not suited for this job. The 80/20 rule applies here, but our situation is a bit better. About half of the people who join stay in the industry for at least a year. Please learn more about the job before you contact me. Please read the two articles I posted earlier for details on the job duties and requirements.

1. Islamic insurance and my career

2. Salaam, what can I do for you?

The regions listed above are provinces where we have branch offices. If you live in these areas, you can contact me for an interview and assessment. If you are in a place where we do not have a branch yet, do not worry. Our company will open new offices throughout the year. Tibet might be the only province-level area without a branch by the end.

Muslim Life Guide Vancouver: MDRT Meeting, Islamic Insurance Ethics and Muslim Professionals

Articles • yusuf908 posted the article • 0 comments • 92 views • 2026-05-22 23:36

Summary: This Muslim life guide from Vancouver covers the MDRT annual meeting, Muslim insurance professionals from different countries, mainland Chinese attendance changes, halal finance discussions, Islamic insurance ethics, Muslim representation in the industry, and reflections on dignity and protection.

Gathering with Muslim Insurance Professionals from Around the World at the MDRT Annual Meeting in Vancouver is presented here as a firsthand travel account in clear English, beginning with this scene: The Million Dollar Round Table (MDRT) started in the United States in 1927. At that time, 32 life insurance agents who sold over one million dollars in policies wanted to form a forum to promote high standards in life. The account keeps its focus on Muslim Travel while preserving the names, places, food, and historical details from the Chinese source.

The Million Dollar Round Table (MDRT) started in the United States in 1927. At that time, 32 life insurance agents who sold over one million dollars in policies wanted to form a forum to promote high standards in life insurance sales and improve the image of insurance professionals.

Since then, the MDRT annual meeting has been held every year in either the United States or Canada. Last year it was in the U.S., and this year it is at the Vancouver Convention Centre in Canada.

Vancouver Convention Centre

This year's attendance is very different from previous years. Before 2019, as the Chinese insurance market grew rapidly, the total number of attendees from mainland China, Hong Kong, and Taiwan was the highest, and it increased every year. This year, however, the Mandarin speakers I saw at the venue were mainly from Taiwan, with a reported attendance of over 600 people. Very few people came from Hong Kong, reportedly fewer than 30. Among the East Asian faces, there were many from Japan and South Korea, while the largest groups from Southeast Asia were from Singapore and Thailand.

The sharp drop in attendees from mainland China may be related to political and economic factors. For one thing, we do not have direct flights to Canada, so most people have to transfer, which takes a long time. Prices in North America have soared in recent years, making a round trip very expensive. On the other hand, many of our colleagues could not get visas. I only saw a single-digit number of colleagues from my own company at the venue, even though over a thousand of us actually met the criteria to attend.

2024 MDRT President Gregory B. Gagne, ChFC

Another objective factor for the sharp decline in mainland attendees is that many large state-owned insurance companies no longer organize trips to the U.S. in an official capacity. Award winners have to go on their own. Instead, they attend insurance award ceremonies held within China, such as the International Management Associate (IMA) awards ceremony I attended last year. Although it is nominally an international award, everyone who attended was an insurance elite from the mainland.

The group in the picture above is the Thai delegation taking a group photo. They are easy to recognize because they are wearing traditional Thai clothing.

This is a delegation of middle-aged Japanese women (obasan). This is just the tip of the iceberg for the Japanese delegation, as the Japanese MDRT is not made up entirely of middle-aged women.

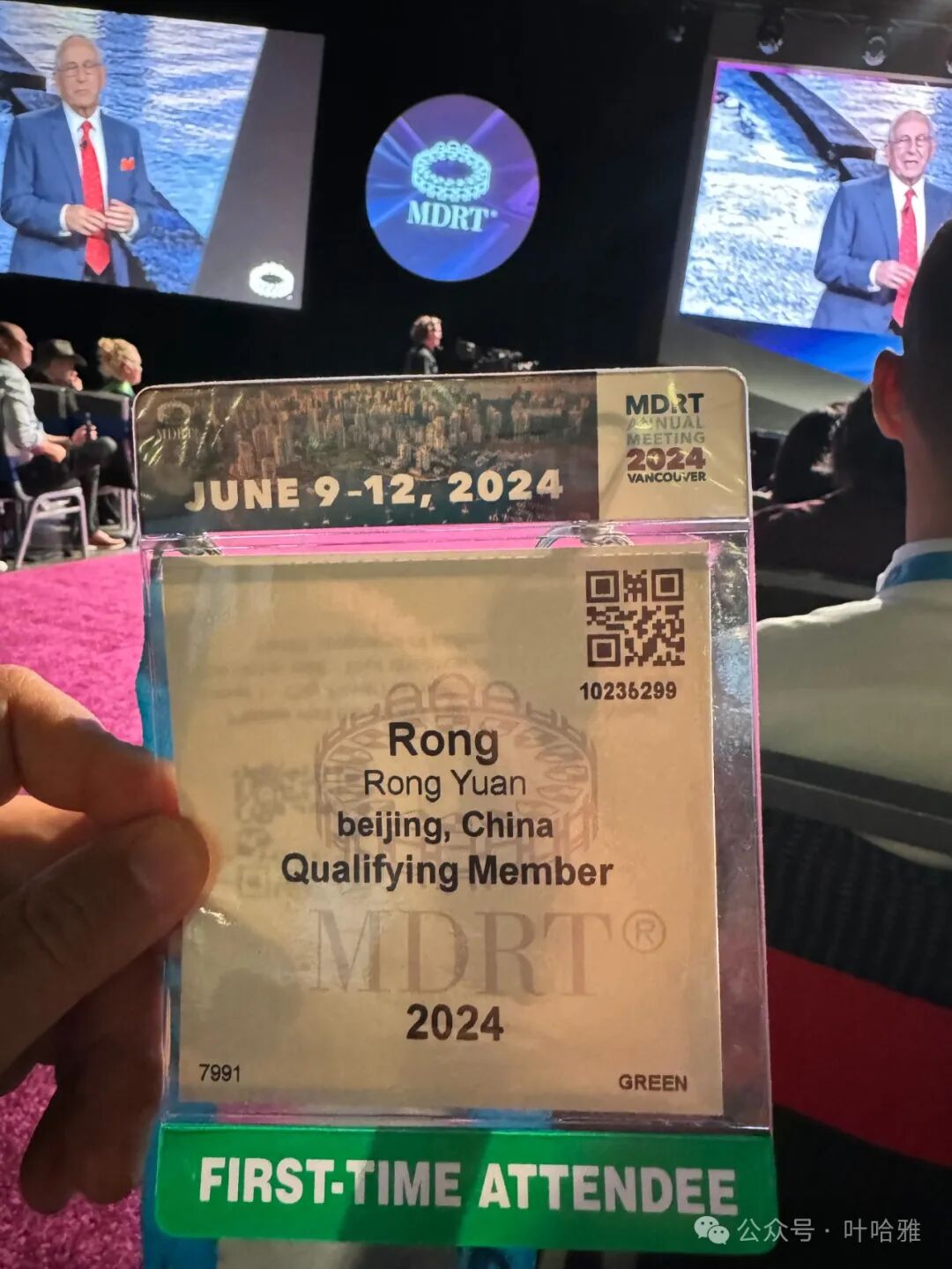

This is my conference badge. You must have it to enter during the meeting. There are guards at the entrance of every venue, so it is hard to sneak in without one. The badges are different every year.

On the first day of the conference, I met this young woman from Jordan. She was easy to recognize because she wore a headscarf. I showed her some articles I translated about Islamic insurance law (sharia), and she was very surprised. She took photos of my articles and translated them into Arabic. It felt amazing to share knowledge about insurance law with an Arab person in this way.

The venue provides simultaneous interpretation services. Everyone gets a small translation device where they can select a language they understand.

These people are all veteran North American members of many years, and the bald man holding the microphone has been a member for over twenty years.

One of the keynote speakers was a person with dwarfism. This was a heartwarming moment for me. MDRT usually invites ordinary people, grassroots elites, rather than celebrities to stand on stage. Each guest shares their personal growth and shows their family life, which makes the audience feel it is real.

The Malaysian MDRT delegation was very warm. The young women asked where I was from. I said I am a Chinese Hui Muslim. They asked which province, and I said I am from Beijing. I showed them photos of my family's Hajj pilgrimage. They were very excited and immediately called over a colleague who spoke Chinese to take a photo with me.

They belong to a Muslim insurance company in Malaysia and asked me if there are any Muslim insurance products in China. I said there are none in mainland China yet, and only a few insurance companies in Hong Kong have Muslim insurance businesses. Perhaps this will open up in the future.

I covered the topic of Muslim insurance in my previous article, Mustafa Zaka: Traditional Commercial Insurance Complies with Sharia.

I introduced it there.

According to current scholars, so-called Muslim insurance is not feasible in practice. This is because there are no Muslim reinsurance companies in the world today that can support Muslim insurance companies. Also, because Muslim insurance adds operating costs to its design, the products are expensive and offer weak coverage, making them uncompetitive in the market. They rely more on the sentiment of the faithful to pay for them, which limits the development of Muslim insurance. Therefore, we should re-evaluate the Sharia regarding traditional insurance and allow Muslims to purchase commercial insurance.

I met a very kind uncle from Singapore. He has worked in insurance for thirty years, and his daughter has been in the industry for nine years. Both father and daughter have achieved Million Dollar Round Table (MDRT) membership. It is a case of a daughter following in her father's footsteps. Many insurance professionals overseas, like this uncle, treat insurance as a lifelong career.

The insurance market in Singapore is different from the mainland. Mainland insurance teams can be very large with no upper limit on members, but in Singapore, you can only form a small team of up to 15 people. Also, there are not many insurance companies in Singapore, so customers have fewer choices and competition is fierce. The uncle has an annual salary of 400,000 Singapore dollars, which is equivalent to over 2 million RMB. This income would rank in the top 100 at my company, but he is very frugal in his daily life. He said that when he meets clients, he just chooses an ordinary coffee shop because he does not want to project an image of being very wealthy.

Besides meeting insurance elites from various countries, I also met two colleagues from my company who live in Canada. Even though their time zone is the complete opposite of China's, it does not stop them from qualifying for the Million Dollar Round Table for many years in a row. This is one of the reasons I chose Mingya, as it allows me to do my job from any corner of the globe.

Both of these colleagues come from wealthy backgrounds, but they still work hard and stay positive. They did not just lie flat while living abroad. You could say that the momentum successful people have makes them unwilling to be mediocre in any environment, leading them to achieve outstanding results.

Every year, MDRT attracts tens of thousands of insurance elites from all over the world, but looking around the venue, the number of Muslims is very small. It is possible that I did not recognize some of the male Muslims, but I expect the number of this group is not very high. This is completely disproportionate to the fact that Muslims make up one-fifth of the world's population.

The people in the blue caps in the photo above are MDRT Jews. Insurance is already widely accepted in Judaism and Christianity, and North America has a very mature insurance industry. A century ago, they used the influence of the church to make insurance a part of daily life. Fortunately, Islamic legal scholars in North America, such as Ibrahim Khan and Monzer Kahf, also have an open attitude toward insurance.

Ibrahim Khan: Is insurance halal?

A collection of fatwa Q&As on insurance by Professor Sheikh Monzer Kahf.

In modern society, insurance has become a necessity. If a person lacks health insurance or retirement insurance, it is hard for them to live a worry-free and decent life. It is easy to issue a religious ruling that bans insurance, but these scholars do not provide alternatives for what to do instead. The difficulties this causes for the lives of Muslims are very real. Becoming an actuary is one of the hardest certifications in the world, taking an average of 10 years to complete. Since insurance is such a complex financial product, how can it be easily declared illegal?

A cruise ship heading to Alaska.

Look at the fundraising links in our social media feeds. When a family is reduced to crowdfunding for medical treatment, they lose their dignity. Relying on online crowdfunding is a form of begging, and begging is a detestable act repeatedly mentioned in the Quran and Sunnah. I do not want to see our community appearing on crowdfunding platforms all the time. As vicegerents on earth, this should not be our image. view all

Summary: This Muslim life guide from Vancouver covers the MDRT annual meeting, Muslim insurance professionals from different countries, mainland Chinese attendance changes, halal finance discussions, Islamic insurance ethics, Muslim representation in the industry, and reflections on dignity and protection.

Gathering with Muslim Insurance Professionals from Around the World at the MDRT Annual Meeting in Vancouver is presented here as a firsthand travel account in clear English, beginning with this scene: The Million Dollar Round Table (MDRT) started in the United States in 1927. At that time, 32 life insurance agents who sold over one million dollars in policies wanted to form a forum to promote high standards in life. The account keeps its focus on Muslim Travel while preserving the names, places, food, and historical details from the Chinese source.

The Million Dollar Round Table (MDRT) started in the United States in 1927. At that time, 32 life insurance agents who sold over one million dollars in policies wanted to form a forum to promote high standards in life insurance sales and improve the image of insurance professionals.

Since then, the MDRT annual meeting has been held every year in either the United States or Canada. Last year it was in the U.S., and this year it is at the Vancouver Convention Centre in Canada.

Vancouver Convention Centre

This year's attendance is very different from previous years. Before 2019, as the Chinese insurance market grew rapidly, the total number of attendees from mainland China, Hong Kong, and Taiwan was the highest, and it increased every year. This year, however, the Mandarin speakers I saw at the venue were mainly from Taiwan, with a reported attendance of over 600 people. Very few people came from Hong Kong, reportedly fewer than 30. Among the East Asian faces, there were many from Japan and South Korea, while the largest groups from Southeast Asia were from Singapore and Thailand.

The sharp drop in attendees from mainland China may be related to political and economic factors. For one thing, we do not have direct flights to Canada, so most people have to transfer, which takes a long time. Prices in North America have soared in recent years, making a round trip very expensive. On the other hand, many of our colleagues could not get visas. I only saw a single-digit number of colleagues from my own company at the venue, even though over a thousand of us actually met the criteria to attend.

2024 MDRT President Gregory B. Gagne, ChFC

Another objective factor for the sharp decline in mainland attendees is that many large state-owned insurance companies no longer organize trips to the U.S. in an official capacity. Award winners have to go on their own. Instead, they attend insurance award ceremonies held within China, such as the International Management Associate (IMA) awards ceremony I attended last year. Although it is nominally an international award, everyone who attended was an insurance elite from the mainland.

The group in the picture above is the Thai delegation taking a group photo. They are easy to recognize because they are wearing traditional Thai clothing.

This is a delegation of middle-aged Japanese women (obasan). This is just the tip of the iceberg for the Japanese delegation, as the Japanese MDRT is not made up entirely of middle-aged women.

This is my conference badge. You must have it to enter during the meeting. There are guards at the entrance of every venue, so it is hard to sneak in without one. The badges are different every year.

On the first day of the conference, I met this young woman from Jordan. She was easy to recognize because she wore a headscarf. I showed her some articles I translated about Islamic insurance law (sharia), and she was very surprised. She took photos of my articles and translated them into Arabic. It felt amazing to share knowledge about insurance law with an Arab person in this way.

The venue provides simultaneous interpretation services. Everyone gets a small translation device where they can select a language they understand.

These people are all veteran North American members of many years, and the bald man holding the microphone has been a member for over twenty years.

One of the keynote speakers was a person with dwarfism. This was a heartwarming moment for me. MDRT usually invites ordinary people, grassroots elites, rather than celebrities to stand on stage. Each guest shares their personal growth and shows their family life, which makes the audience feel it is real.

The Malaysian MDRT delegation was very warm. The young women asked where I was from. I said I am a Chinese Hui Muslim. They asked which province, and I said I am from Beijing. I showed them photos of my family's Hajj pilgrimage. They were very excited and immediately called over a colleague who spoke Chinese to take a photo with me.

They belong to a Muslim insurance company in Malaysia and asked me if there are any Muslim insurance products in China. I said there are none in mainland China yet, and only a few insurance companies in Hong Kong have Muslim insurance businesses. Perhaps this will open up in the future.

I covered the topic of Muslim insurance in my previous article, Mustafa Zaka: Traditional Commercial Insurance Complies with Sharia.

I introduced it there.

According to current scholars, so-called Muslim insurance is not feasible in practice. This is because there are no Muslim reinsurance companies in the world today that can support Muslim insurance companies. Also, because Muslim insurance adds operating costs to its design, the products are expensive and offer weak coverage, making them uncompetitive in the market. They rely more on the sentiment of the faithful to pay for them, which limits the development of Muslim insurance. Therefore, we should re-evaluate the Sharia regarding traditional insurance and allow Muslims to purchase commercial insurance.

I met a very kind uncle from Singapore. He has worked in insurance for thirty years, and his daughter has been in the industry for nine years. Both father and daughter have achieved Million Dollar Round Table (MDRT) membership. It is a case of a daughter following in her father's footsteps. Many insurance professionals overseas, like this uncle, treat insurance as a lifelong career.

The insurance market in Singapore is different from the mainland. Mainland insurance teams can be very large with no upper limit on members, but in Singapore, you can only form a small team of up to 15 people. Also, there are not many insurance companies in Singapore, so customers have fewer choices and competition is fierce. The uncle has an annual salary of 400,000 Singapore dollars, which is equivalent to over 2 million RMB. This income would rank in the top 100 at my company, but he is very frugal in his daily life. He said that when he meets clients, he just chooses an ordinary coffee shop because he does not want to project an image of being very wealthy.

Besides meeting insurance elites from various countries, I also met two colleagues from my company who live in Canada. Even though their time zone is the complete opposite of China's, it does not stop them from qualifying for the Million Dollar Round Table for many years in a row. This is one of the reasons I chose Mingya, as it allows me to do my job from any corner of the globe.

Both of these colleagues come from wealthy backgrounds, but they still work hard and stay positive. They did not just lie flat while living abroad. You could say that the momentum successful people have makes them unwilling to be mediocre in any environment, leading them to achieve outstanding results.

Every year, MDRT attracts tens of thousands of insurance elites from all over the world, but looking around the venue, the number of Muslims is very small. It is possible that I did not recognize some of the male Muslims, but I expect the number of this group is not very high. This is completely disproportionate to the fact that Muslims make up one-fifth of the world's population.

The people in the blue caps in the photo above are MDRT Jews. Insurance is already widely accepted in Judaism and Christianity, and North America has a very mature insurance industry. A century ago, they used the influence of the church to make insurance a part of daily life. Fortunately, Islamic legal scholars in North America, such as Ibrahim Khan and Monzer Kahf, also have an open attitude toward insurance.

Ibrahim Khan: Is insurance halal?

A collection of fatwa Q&As on insurance by Professor Sheikh Monzer Kahf.

In modern society, insurance has become a necessity. If a person lacks health insurance or retirement insurance, it is hard for them to live a worry-free and decent life. It is easy to issue a religious ruling that bans insurance, but these scholars do not provide alternatives for what to do instead. The difficulties this causes for the lives of Muslims are very real. Becoming an actuary is one of the hardest certifications in the world, taking an average of 10 years to complete. Since insurance is such a complex financial product, how can it be easily declared illegal?

A cruise ship heading to Alaska.

Look at the fundraising links in our social media feeds. When a family is reduced to crowdfunding for medical treatment, they lose their dignity. Relying on online crowdfunding is a form of begging, and begging is a detestable act repeatedly mentioned in the Quran and Sunnah. I do not want to see our community appearing on crowdfunding platforms all the time. As vicegerents on earth, this should not be our image.

Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance

Articles • yusuf908 posted the article • 0 comments • 76 views • 2026-05-22 09:39

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.

Insurance brokers need high personal standards. People who cannot think for themselves or learn quickly are not suited for this job. The 80/20 rule applies here, but our situation is a bit better. About half of the people who join stay in the industry for at least a year. Please learn more about the job before you contact me. Please read the two articles I posted earlier for details on the job duties and requirements.

1. Islamic insurance and my career

2. Salaam, what can I do for you?

The regions listed above are provinces where we have branch offices. If you live in these areas, you can contact me for an interview and assessment. If you are in a place where we do not have a branch yet, do not worry. Our company will open new offices throughout the year. Tibet might be the only province-level area without a branch by the end. view all

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.

Insurance brokers need high personal standards. People who cannot think for themselves or learn quickly are not suited for this job. The 80/20 rule applies here, but our situation is a bit better. About half of the people who join stay in the industry for at least a year. Please learn more about the job before you contact me. Please read the two articles I posted earlier for details on the job duties and requirements.

1. Islamic insurance and my career

2. Salaam, what can I do for you?

The regions listed above are provinces where we have branch offices. If you live in these areas, you can contact me for an interview and assessment. If you are in a place where we do not have a branch yet, do not worry. Our company will open new offices throughout the year. Tibet might be the only province-level area without a branch by the end.

Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices

Articles • yusuf908 posted the article • 0 comments • 106 views • 2026-05-21 20:43

Summary: Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices is presented here as a clear English account for Muslim readers, beginning with this scene: There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever. The article keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Islamic Insurance, Takaful, Muslim Finance.

Islamic finance books that can be sold publicly in mainland China.

There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever judges incorrectly must bear the consequences.

Currently, scholars have three views on insurance. The first considers insurance haram (forbidden), the second considers it lawful, and the third is a middle ground, suggesting the insurance system needs reform to remove its unlawful parts.

Scholars who view insurance as unlawful argue that it contains elements of interest and gambling. They believe insurance involves interest because life insurance contracts promise a fixed payout at a set time, which carries the suspicion of interest. Health insurance contracts are uncertain about when a payout will occur, as it only happens if the client faces a loss, and this uncertainty carries the suspicion of gambling.

It is undeniable that interest and gambling are explicitly forbidden in the Quran. The Quran mentions the prohibition of interest four times: Surah Ar-Rum verse 39, Surah An-Nisa verse 161, Surah Al-Imran verses 130-132, and Surah Al-Baqarah verses 275-281.

Whatever you give for interest to increase within the wealth of people will not increase with Allah. But what you give in charity, desiring the countenance of Allah—those are the multipliers. (Surah Ar-Rum, verse 39)

The schools of jurisprudence have slight differences regarding interest. For example, regarding interest on debt, all four major schools agree that any loan that brings a benefit involves interest. However, Ibn Hazm mentions in his book Al-Muhalla that interest is not allowed in sales or deferred payments, except for six items: gold, silver, wheat, barley, dates, and salt. But for loans, interest is allowed for any commodity. The basis for this is a Hadith narrated by Abu Hurairah: The best among you is the one who is best in repayment. However, there are different opinions regarding this Hadith, as other Hadiths mention: Gold for gold, silver for silver.

Regarding the views of the four major schools of jurisprudence on interest, I will only cite their views on the exchange of goods that cannot be calculated, measured, or weighed:

1. Hanafi school: Profit is allowed in both spot transactions and deferred transactions.

2. Shafi'i school: Profit is allowed in both spot transactions and deferred transactions.

3. Maliki school: Deferred transactions are not allowed even without profit, but profit is allowed in spot transactions.

4. Hanbali school: Profit is allowed in both spot transactions and deferred transactions.

Imam Abu Hanifa, the founder of the Hanafi school, allowed Muslims to enter non-Muslim territories and trade based on interest. He also allowed Muslims to trade on a similar interest-based model with people who converted to Islam from non-Islamic countries. This means that for Muslims, receiving interest is illegal, but paying interest is not. However, the Shafi'i, Maliki, and Hanbali schools all disagree with the Hanafi view.

I am quoting the views of scholars not to prove that interest is legal. On the contrary, I firmly believe that interest is

illegal, no matter what form it takes. I just find that in modern society, it is impossible for us to avoid getting the dust of interest on us. As long as we use banks in our daily lives, we will inevitably have a relationship with interest. Even the companies we work for pay our salaries through banks, and the company's operating income deposited in banks will inevitably generate interest. If we want to completely cut off interest, we can only isolate ourselves from the world.

Ibn Mas'ud narrated that the Prophet said: 'Before the Day of Judgment, interest will be widespread.' 'Signs of the End Times' by Yusuf al-Wabil. Al-Mundhiri considered the narrators of this hadith to be reliable.

Abu Hurairah narrated that the Messenger of Allah said: 'A time will come when everyone will consume interest. Even if someone does not consume it, they will still be touched by the dust of interest.' 'Sunan Abu Dawood', Hadith 3331.

Such days have already arrived. The social pension insurance that the state mandates can be seen as an extension of interest, as we receive monthly payments after retirement. Who living in a city can avoid this? If we do not rely on pension insurance, how will we live when we get old? We can only rely on our children for support, but how can we guarantee our children's future lives? Besides, there are also elderly people who have no children.

Let's discuss another controversy in insurance: is buying insurance equivalent to gambling?

They ask you about the ruling on wine and gambling. Say: 'In both there is great sin, and some benefit for people, but the sin of them is greater than their benefit.' (Surah Al-Baqarah, verse 219)

Gambling is illegal in most countries, and Islam is no exception. Some scholars argue that gambling is forbidden because of uncertainty, but everyone knows gambling ruins families and encourages people to get something for nothing. People gamble to make a profit without putting in real work, which feeds human greed. This is the real reason Islam forbids it, not just because of uncertainty. Strictly speaking, gambling results are not truly uncertain; they are just too complex for the average person to predict, though they can be calculated with advanced technology.

Insurance contracts clearly state when a claim can be made and for how long the policy lasts. This provides a service of protection. Even if we do not know when a risk will happen, the protection is always there. It is like paying for a bodyguard who only steps in when you are in danger. Does the fact that we do not know when danger will strike mean hiring a bodyguard is the same as gambling?

Buying insurance does not make a person go bankrupt. Insurance companies usually do not accept applications for coverage that exceeds a person's assets. They check the applicant's qualifications first. This is fundamentally different from gambling, which allows anyone to participate without restrictions. It is very hard to make a profit from insurance. When a risk event happens, it usually comes with the cost of a person's health or life. Intentionally committing insurance fraud is illegal, which is another fundamental difference between insurance and gambling.

Think about the rules against alcohol. Islam forbids alcohol because getting drunk makes people lose their reason and affects things like namaz. This leads to the ruling that anything that intoxicates is forbidden. Things that cause intoxication include alcohol in food and other narcotics. Ancient people did not know about chemical alcohol. When the alcohol content in a drink reaches a certain level, it makes you drunk. But chemistry students know that almost all fruit contains alcohol, and the riper the fruit, the higher the content. It is almost impossible to strictly forbid any trace of alcohol in food. That is why international halal food standards allow for tiny amounts of alcohol. I have discussed this in my article about non-halal foods mentioned in the scriptures. Already written.

So, the uncertainty in insurance is like the tiny amount of alcohol in food. It is hard to avoid and does not need to be avoided. We face many uncertain things in life. Uncertainty is not wrong as long as it does not harm anyone.

I also want to live in a place that is entirely lawful and away from controversial things. But think about it: for an average family, if they do not buy insurance, what better way is there to help them get through a crisis when a risk occurs? Should they ask for charity (niyat) in person or use online crowdfunding? Both are forms of begging, which the Hadith repeatedly discourages. I have written an article about the scriptures regarding begging, which you can read in my piece about being a Muslim who never begs, just like the Kazakh people.

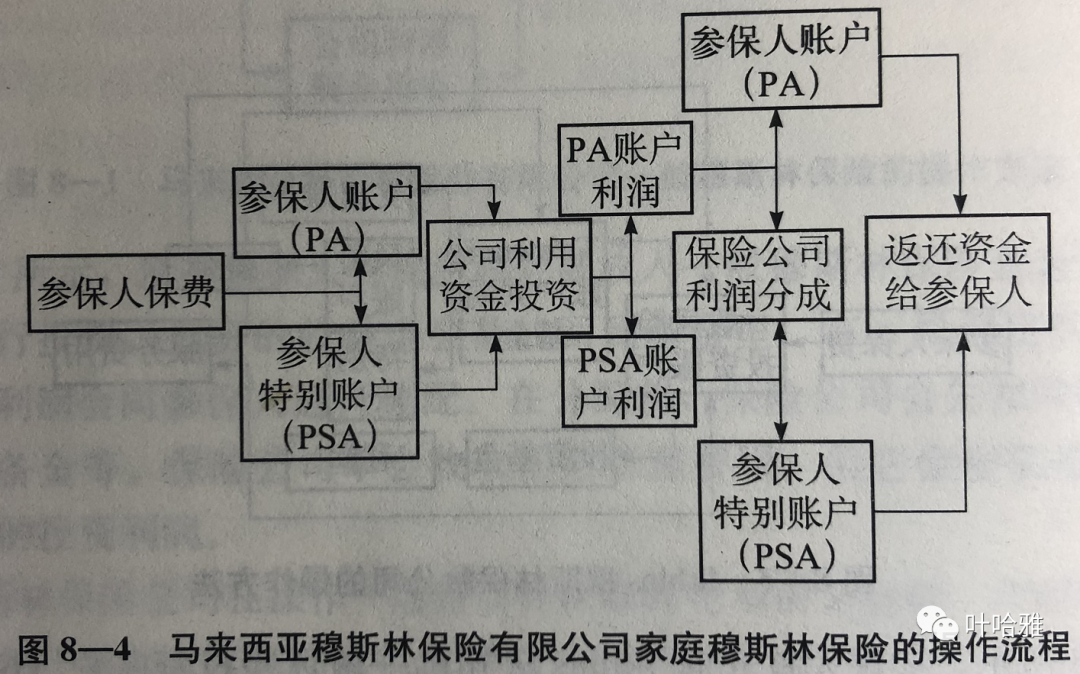

Finally, let us look at how Muslim insurance companies work. All Muslim insurance operators in Malaysia provide Muslim insurance services. If you buy a policy there, the contract requires you to pay a premium and also contribute a portion of money as a donation to help others hit by disaster. All premiums are put into a Muslim insurance fund. The company invests this money, and the profits go back into the fund. When the policy matures, the profits are distributed to the policyholders, and the insurance company deducts its fees to make a profit.

Screenshot from Islamic Banking and Financial Systems.

The way these Muslim insurance companies work is basically the same as the insurance companies in our country. The only difference is that Muslim insurance companies divide the premiums into different categories, and they do not invest in non-halal projects like alcohol. But from the customer's experience, both involve paying a premium to get protection. In this sense, the principle is the same for both types of insurance.

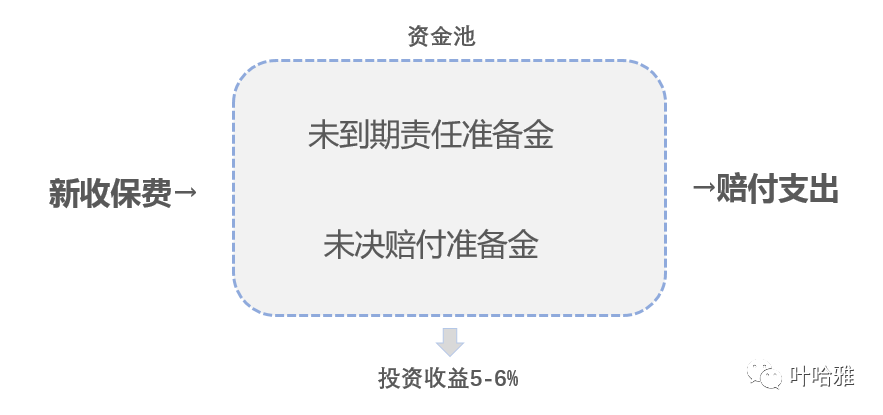

Capital flow of traditional insurance companies.

We can see that traditional insurance companies also split premiums into two parts after collecting them. One part is used as a reserve for emergencies, and the other is invested. The difference is that they are not Muslim insurance companies, so they are not restricted in where they can invest.

That is all I can think of for now regarding Islamic insurance. I hope my article helps clear up your questions. I am not trying to convince everyone. If you do not agree with insurance, you can just take responsibility for your own risks. Everyone should be responsible for their own actions. If you are interested in this, you can look at my previous posts about Islamic insurance and my career. view all

Summary: Muslim Friendly China: Islamic Insurance, Takaful, Faith and Everyday Financial Choices is presented here as a clear English account for Muslim readers, beginning with this scene: There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever. The article keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Islamic Insurance, Takaful, Muslim Finance.

Islamic finance books that can be sold publicly in mainland China.

There is a recognized principle in Islamic jurisprudence: to declare something forbidden, one must provide evidence from the Quran or Hadith. Otherwise, one cannot easily label a lawful thing as forbidden, and whoever judges incorrectly must bear the consequences.

Currently, scholars have three views on insurance. The first considers insurance haram (forbidden), the second considers it lawful, and the third is a middle ground, suggesting the insurance system needs reform to remove its unlawful parts.

Scholars who view insurance as unlawful argue that it contains elements of interest and gambling. They believe insurance involves interest because life insurance contracts promise a fixed payout at a set time, which carries the suspicion of interest. Health insurance contracts are uncertain about when a payout will occur, as it only happens if the client faces a loss, and this uncertainty carries the suspicion of gambling.

It is undeniable that interest and gambling are explicitly forbidden in the Quran. The Quran mentions the prohibition of interest four times: Surah Ar-Rum verse 39, Surah An-Nisa verse 161, Surah Al-Imran verses 130-132, and Surah Al-Baqarah verses 275-281.

Whatever you give for interest to increase within the wealth of people will not increase with Allah. But what you give in charity, desiring the countenance of Allah—those are the multipliers. (Surah Ar-Rum, verse 39)

The schools of jurisprudence have slight differences regarding interest. For example, regarding interest on debt, all four major schools agree that any loan that brings a benefit involves interest. However, Ibn Hazm mentions in his book Al-Muhalla that interest is not allowed in sales or deferred payments, except for six items: gold, silver, wheat, barley, dates, and salt. But for loans, interest is allowed for any commodity. The basis for this is a Hadith narrated by Abu Hurairah: The best among you is the one who is best in repayment. However, there are different opinions regarding this Hadith, as other Hadiths mention: Gold for gold, silver for silver.

Regarding the views of the four major schools of jurisprudence on interest, I will only cite their views on the exchange of goods that cannot be calculated, measured, or weighed:

1. Hanafi school: Profit is allowed in both spot transactions and deferred transactions.

2. Shafi'i school: Profit is allowed in both spot transactions and deferred transactions.

3. Maliki school: Deferred transactions are not allowed even without profit, but profit is allowed in spot transactions.

4. Hanbali school: Profit is allowed in both spot transactions and deferred transactions.

Imam Abu Hanifa, the founder of the Hanafi school, allowed Muslims to enter non-Muslim territories and trade based on interest. He also allowed Muslims to trade on a similar interest-based model with people who converted to Islam from non-Islamic countries. This means that for Muslims, receiving interest is illegal, but paying interest is not. However, the Shafi'i, Maliki, and Hanbali schools all disagree with the Hanafi view.

I am quoting the views of scholars not to prove that interest is legal. On the contrary, I firmly believe that interest is

illegal, no matter what form it takes. I just find that in modern society, it is impossible for us to avoid getting the dust of interest on us. As long as we use banks in our daily lives, we will inevitably have a relationship with interest. Even the companies we work for pay our salaries through banks, and the company's operating income deposited in banks will inevitably generate interest. If we want to completely cut off interest, we can only isolate ourselves from the world.

Ibn Mas'ud narrated that the Prophet said: 'Before the Day of Judgment, interest will be widespread.' 'Signs of the End Times' by Yusuf al-Wabil. Al-Mundhiri considered the narrators of this hadith to be reliable.

Abu Hurairah narrated that the Messenger of Allah said: 'A time will come when everyone will consume interest. Even if someone does not consume it, they will still be touched by the dust of interest.' 'Sunan Abu Dawood', Hadith 3331.

Such days have already arrived. The social pension insurance that the state mandates can be seen as an extension of interest, as we receive monthly payments after retirement. Who living in a city can avoid this? If we do not rely on pension insurance, how will we live when we get old? We can only rely on our children for support, but how can we guarantee our children's future lives? Besides, there are also elderly people who have no children.

Let's discuss another controversy in insurance: is buying insurance equivalent to gambling?

They ask you about the ruling on wine and gambling. Say: 'In both there is great sin, and some benefit for people, but the sin of them is greater than their benefit.' (Surah Al-Baqarah, verse 219)

Gambling is illegal in most countries, and Islam is no exception. Some scholars argue that gambling is forbidden because of uncertainty, but everyone knows gambling ruins families and encourages people to get something for nothing. People gamble to make a profit without putting in real work, which feeds human greed. This is the real reason Islam forbids it, not just because of uncertainty. Strictly speaking, gambling results are not truly uncertain; they are just too complex for the average person to predict, though they can be calculated with advanced technology.

Insurance contracts clearly state when a claim can be made and for how long the policy lasts. This provides a service of protection. Even if we do not know when a risk will happen, the protection is always there. It is like paying for a bodyguard who only steps in when you are in danger. Does the fact that we do not know when danger will strike mean hiring a bodyguard is the same as gambling?

Buying insurance does not make a person go bankrupt. Insurance companies usually do not accept applications for coverage that exceeds a person's assets. They check the applicant's qualifications first. This is fundamentally different from gambling, which allows anyone to participate without restrictions. It is very hard to make a profit from insurance. When a risk event happens, it usually comes with the cost of a person's health or life. Intentionally committing insurance fraud is illegal, which is another fundamental difference between insurance and gambling.

Think about the rules against alcohol. Islam forbids alcohol because getting drunk makes people lose their reason and affects things like namaz. This leads to the ruling that anything that intoxicates is forbidden. Things that cause intoxication include alcohol in food and other narcotics. Ancient people did not know about chemical alcohol. When the alcohol content in a drink reaches a certain level, it makes you drunk. But chemistry students know that almost all fruit contains alcohol, and the riper the fruit, the higher the content. It is almost impossible to strictly forbid any trace of alcohol in food. That is why international halal food standards allow for tiny amounts of alcohol. I have discussed this in my article about non-halal foods mentioned in the scriptures. Already written.

So, the uncertainty in insurance is like the tiny amount of alcohol in food. It is hard to avoid and does not need to be avoided. We face many uncertain things in life. Uncertainty is not wrong as long as it does not harm anyone.

I also want to live in a place that is entirely lawful and away from controversial things. But think about it: for an average family, if they do not buy insurance, what better way is there to help them get through a crisis when a risk occurs? Should they ask for charity (niyat) in person or use online crowdfunding? Both are forms of begging, which the Hadith repeatedly discourages. I have written an article about the scriptures regarding begging, which you can read in my piece about being a Muslim who never begs, just like the Kazakh people.

Finally, let us look at how Muslim insurance companies work. All Muslim insurance operators in Malaysia provide Muslim insurance services. If you buy a policy there, the contract requires you to pay a premium and also contribute a portion of money as a donation to help others hit by disaster. All premiums are put into a Muslim insurance fund. The company invests this money, and the profits go back into the fund. When the policy matures, the profits are distributed to the policyholders, and the insurance company deducts its fees to make a profit.

Screenshot from Islamic Banking and Financial Systems.

The way these Muslim insurance companies work is basically the same as the insurance companies in our country. The only difference is that Muslim insurance companies divide the premiums into different categories, and they do not invest in non-halal projects like alcohol. But from the customer's experience, both involve paying a premium to get protection. In this sense, the principle is the same for both types of insurance.

Capital flow of traditional insurance companies.

We can see that traditional insurance companies also split premiums into two parts after collecting them. One part is used as a reserve for emergencies, and the other is invested. The difference is that they are not Muslim insurance companies, so they are not restricted in where they can invest.

That is all I can think of for now regarding Islamic insurance. I hope my article helps clear up your questions. I am not trying to convince everyone. If you do not agree with insurance, you can just take responsibility for your own risks. Everyone should be responsible for their own actions. If you are interested in this, you can look at my previous posts about Islamic insurance and my career.

Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance

Articles • yusuf908 posted the article • 0 comments • 61 views • 2026-05-24 00:17

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.

Insurance brokers need high personal standards. People who cannot think for themselves or learn quickly are not suited for this job. The 80/20 rule applies here, but our situation is a bit better. About half of the people who join stay in the industry for at least a year. Please learn more about the job before you contact me. Please read the two articles I posted earlier for details on the job duties and requirements.

1. Islamic insurance and my career

2. Salaam, what can I do for you?

The regions listed above are provinces where we have branch offices. If you live in these areas, you can contact me for an interview and assessment. If you are in a place where we do not have a branch yet, do not worry. Our company will open new offices throughout the year. Tibet might be the only province-level area without a branch by the end. view all

Summary: Muslim Life Guide China: Ramadan Career Wins, Faith-Friendly Work and Islamic Insurance is presented here as a clear English account for Muslim readers, starting with this scene: Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards. It keeps the original names, food details, mosque details, photographs, and cultural context while focusing on Ramadan Life, Muslim Careers, Islamic Insurance.

Ramadan is a month of harvest, and good deeds performed during this time receive double the reward. April was also a month of professional harvest for me. Due to the recurring pandemic last year, our company's 2020 awards ceremonies were delayed until this month.

At the recent 2020 annual meeting, I was honored to receive a promotion certificate and become a company partner. Our career ranks go from consultant to agent, senior agent, veteran agent, and finally partner. Reaching the partner level means a significant income increase and eligibility for year-end dividends, which is rare among top brokerage firms.

Me on stage receiving the award.

I also won an award for being in the top ten for annual insurance policy volume in our business department. I feel very honored to achieve this among nearly a thousand people. In 2020, I sold over 200 insurance policies, covering medical, critical illness, accident, and group insurance from more than twenty companies. My clients are across the country, with the furthest in Xinjiang and Guangdong. Thanks to the rapid development of internet insurance, we can complete applications without leaving home.

Top ten in annual policy volume.

I was also invited by the training department to be a guest lecturer for new recruits, sharing my work experience multiple times. Mingya has many talented people, so becoming a lecturer is an honor.

Promotional poster made by the training department.

Of course, I often used these training opportunities to sneak in some basic knowledge I teach.

Promotional poster made by the training department.

Reporting my work results to you, I want to say that work and faith can be combined organically. Faith has not been a burden on my work; instead, it has improved my efficiency to some extent. This year's Ramadan has been extra easy. My work is flexible with no need to clock in, and I do most of it at home on my computer. Also, Ramadan is shifting toward winter, so days are shorter and the weather is cooler. It is not like a few years ago when Ramadan was in midsummer, so fasting is stress-free.

In my previous job, I always had to find excuses to slip out for Friday namaz. Company social events always involved drinking, and I felt out of place sitting there, forced to put on a fake smile. Now I have no such worries. My work does not require me to suck up to leaders; all promotions and awards are based on performance. No one interferes with anyone else. My relationship with colleagues is more like college classmates; we hang out if we want, or we can be alone. Even when I achieve results, if I attend a team-building event, the organizer arranges halal food for me, even if I am the only Hui Muslim there. Now, the Hongbinlou restaurant downstairs has become one of our designated spots for team building.

Many colleagues started following my public account after my training sessions and learned about halal food. For most Han Chinese colleagues, it opened a new world. Some have even become interested in fasting and joined our activities to experience hunger, though their current motivation is mostly to lose weight.

I think I have found a career for life. It is a sunrise industry. Many people are just starting to understand insurance brokers. The definition of an insurance broker was written into the Insurance Law of the People's Republic of China long ago. It has been around for over a hundred years abroad, but only seventeen years in China. Seventeen years is also our company's age, as we were the first to introduce the brokerage model to China.

This profession has no ceiling and unlimited income, which is important for ambitious people. Many jobs hit a wall after 35, with no room for promotion or salary growth. Insurance brokers can keep moving up; your career grows as high as your ability allows.

I have told my team many times that being an insurance broker with a million-yuan annual salary in China is the happiest thing. You do not need to suck up to the powerful, there is no complex office politics, your income is clean, you live freely, and you can balance family and career. In 2019, our company had 179 brokers earning over a million. In 2020, even with the severe pandemic, that number grew to 208. This is the advantage of being an insurance broker. We use online methods to compare products and get the best insurance plans for clients, so the pandemic is not scary for us.

This year, my direct team has grown to 17 members in Ningxia, Jiangsu, Anhui, and Beijing. I have not met the ones in other cities, but that does not stop us from being a team. Our company's basic law encourages building teams across regions, and I have introduced some outstanding team members on my public account.

Team member 1: The slash-career life of Shadian Duosi.

Team member 2: The Plan B of a Hui Muslim master's student from Minzu University of China.

Team member 3: This Hui Muslim girl from Hohhot is truly excellent.